This post examines why explainable AI has become a non-negotiable requirement in credit risk, not as a theoretical ideal but as a legal, operational, and competitive reality. It covers:

• Why regulators now treat unexplainable credit models as compliance violations, with enforcement actions reaching tens of millions of dollars

• The real-world cases, from the Apple Card investigation to the Massachusetts AI lending settlement, that demonstrate what happens when black-box models make credit decisions they cannot justify

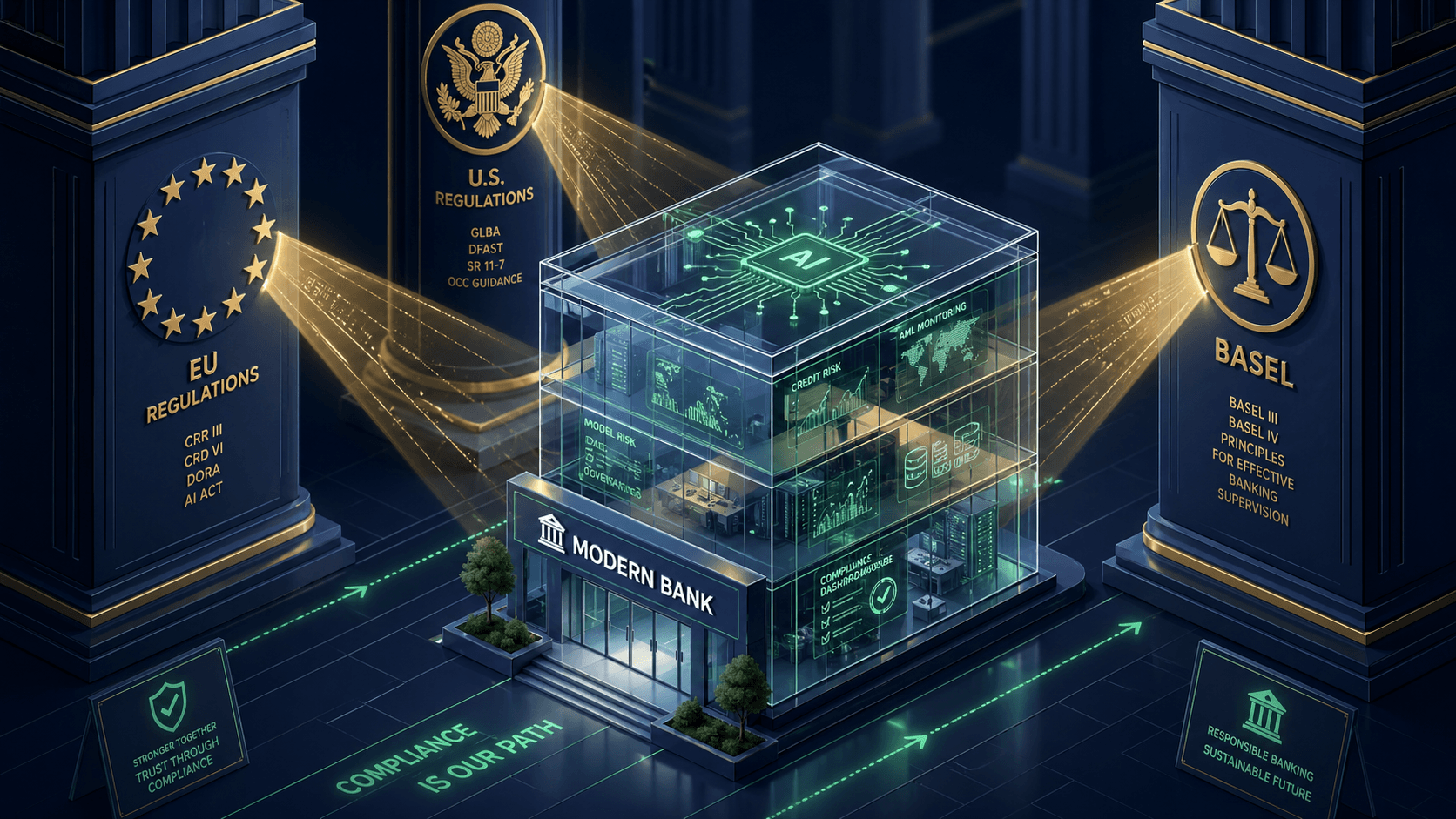

• The multi-jurisdictional regulatory framework that banks must navigate, spanning the EU AI Act, FCRA and ECOA, ECB supervisory expectations, Federal Reserve SR 11-7, and Basel Committee guidance

• The technical solutions available today, including SHAP, LIME, counterfactual explanations, and Explainable Boosting Machines, along with the evidence that interpretable models can match black-box accuracy

• The governance challenge that most banks have not solved: making explainability work across development, validation, and audit

• Why compliance is also competitive advantage, and what the next wave of regulatory expectations will demand

If your organisation deploys AI in lending, underwriting, or credit decisioning, the question is no longer whether to build explainability into your systems. The question is how quickly you can do it before regulators, customers, and competitors force the issue.

The Existential Problem: Why Black Boxes in Credit Risk Cannot Survive

In October 2024, the Consumer Financial Protection Bureau fined Apple $25 million and Goldman Sachs $45 million for failures related to the Apple Card credit programme. The core issue was not that the algorithms discriminated intentionally. It was that the algorithms made credit limit decisions that neither the bank nor its customer service agents could explain. When regulators asked why one applicant received a $20,000 limit while a spouse with identical finances received $1,000, nobody could answer.

That inability to explain was enough. The CFPB's position on the matter was unambiguous: lenders cannot justify noncompliance with fair lending laws based on the complexity or opacity of their technology. The exact phrasing from the Bureau's August 2024 guidance left no room for interpretation: there are no exceptions for new technologies.

This was not an isolated enforcement action. In July 2025, the Massachusetts Attorney General settled a $2.5 million case against a student loan company whose AI underwriting model had produced unlawful disparate impact based on race and immigration status. The company had failed to test its algorithmic models for bias. The settlement required not just the fine but the construction of an entirely new governance system for fair lending testing and controls.

These cases mark an inflection point. For decades, credit risk modelling operated under an implicit assumption: if the model was accurate, the details of how it reached its decisions were secondary concerns. That assumption is now regulatory liability. Across the United States and the European Union, regulators have converged on a single requirement. If an AI system makes or influences credit decisions, the institution deploying it must be able to explain those decisions in terms that consumers, auditors, and supervisors can understand.

The Fair Credit Reporting Act requires creditors to provide specific reasons when they take adverse action on a credit application. The Equal Credit Opportunity Act reinforces this by prohibiting discrimination and requiring that credit decisions be explainable. These are not new laws. They have been in force for decades. What has changed is the technology: machine learning models that are orders of magnitude more complex than the logistic regression scorecards these laws were originally designed to govern.

As we examined in our analysis of why explainable AI matters more than most practitioners realise, the gap between what these models can predict and what they can explain is where legal exposure lives. The CFPB, the ECB, and the Basel Committee have all signalled that this gap will not be tolerated. The institutions that close it first will lead the next era of credit risk management. Those that do not will face fines, reputational damage, and competitive disadvantage.

When Opacity Becomes Discrimination: The Cases That Changed Everything

Enforcement actions and investigations tell a clearer story than policy documents alone. Three recent cases illustrate how black-box credit models create legal exposure, not through intentional discrimination, but through the inability to prove that discrimination is absent.

The Apple Card Investigation

When Apple launched its credit card with Goldman Sachs in 2019, the product was marketed as a breakthrough in consumer finance. Within months, it became the most high-profile case of AI bias in lending. David Heinemeier Hansson, co-creator of Ruby on Rails, reported that he was offered twenty times the credit limit of his wife, despite the couple sharing all their financial assets. Steve Wozniak reported a similar experience: his wife received a dramatically lower limit despite having a higher credit score.

The New York Department of Financial Services launched an investigation and found that Goldman Sachs relied on algorithms and machine learning for credit decision-making, but that customer service agents could not explain the algorithms or the basis for credit limit differences. The investigation did not find unlawful discrimination in the technical legal sense. What it found was arguably worse for the industry: a major financial institution deploying credit models it could not explain, even to its own staff.

The October 2024 CFPB enforcement action imposed $70 million in combined fines. The message was clear: algorithmic opacity is not a defence. It is an admission that governance has failed.

The Massachusetts AI Lending Settlement

In July 2025, a student loan company settled with the Massachusetts Attorney General for $2.5 million after its AI underwriting model produced unlawful disparate impact. The model used a metric called the Cohort Default Rate as a variable in credit decisions. This metric, which measures default rates at educational institutions, disproportionately penalised applicants who had attended Historically Black Colleges and Universities. The result: Black and Hispanic applicants were more likely to be denied credit or offered worse terms.

The critical finding was not that the company intended to discriminate. It was that the company had failed to test its algorithmic models for disparate impact. Under fair lending law, intent is not required. If a facially neutral policy produces discriminatory outcomes and the institution cannot demonstrate a legitimate business necessity, the policy violates the law. The settlement required the company to build an entirely new governance system for fair lending testing and algorithmic controls.

The Lehigh University Study: Bias Embedded in Language Models

A 2025 study from Lehigh University tested commercial large language models on identical loan applications where only the applicant's race varied. The results confirmed what regulators had warned about: models recommended denying more loans to Black applicants and charged higher interest rates compared to identical applications from White applicants. Attempts to mitigate this bias through legalistic instructions were largely ineffective. Simple instructions to avoid bias performed better than complex legal prompts.

This study matters because it demonstrates that bias in credit AI is not limited to traditional machine learning models. Large language models, increasingly being explored for lending applications, inherit the same historical biases from their training data. Without explicit controls and testing, these biases reproduce discrimination at scale.

Taken together, these cases establish a pattern. Black-box credit models do not just create theoretical risk. They create measurable legal liability, quantifiable fines, and documented discrimination. As we explored in our analysis of interpretable versus black-box models, the accuracy argument that once justified opacity no longer holds up against the regulatory and ethical costs of unexplainable decisions.

The Regulatory Gauntlet: What Banks Must Comply With

Banks deploying AI credit models face a layered regulatory regime that spans jurisdictions and supervisory bodies. The requirements differ in specifics, but they converge on a single principle: if an AI system influences credit decisions, its outputs must be explainable. There is no jurisdiction where opacity is acceptable.

United States: FCRA, ECOA, and CFPB Enforcement

The Fair Credit Reporting Act Section 615 requires creditors to disclose specific reasons when they take adverse action on a credit application. The Equal Credit Opportunity Act and its implementing regulation, Regulation B, reinforce this by requiring that creditors explain credit decisions regardless of the technology used to make them. These requirements apply to every model, from a simple scorecard to a deep neural network.

The CFPB's 2024 guidance made the application to AI explicit. The Bureau stated that a creditor cannot justify noncompliance based on the mere fact that the technology it employs is too complicated or opaque to understand. The Bureau further noted that courts have already held that an institution's decision to use algorithmic or machine learning tools can itself constitute a policy that produces bias under disparate impact theory.

The practical implication is significant. Adverse action notices must provide specific reasons for denial that a consumer can understand and act upon. A notice stating that the model assigned a low score is not sufficient. The institution must identify which factors, such as debt-to-income ratio, credit utilisation, or payment history, drove the decision. Black-box models that cannot decompose their outputs into interpretable factors cannot satisfy this requirement.

European Union: The AI Act and High-Risk Classification

The EU AI Act classifies credit scoring systems as high-risk under Annex III, specifically because these systems determine access to financial resources and essential services including housing, electricity, and telecommunications. As we detailed in our analysis of what the EU AI Act means for business and innovation, this classification triggers a comprehensive set of requirements.

High-risk AI systems used in credit scoring must implement mandatory risk management systems, produce technical documentation, establish human oversight mechanisms, meet data governance requirements, undergo conformity assessment, register in the EU database, and maintain ongoing incident monitoring. The conformity assessment for credit scoring is an internal self-assessment rather than third-party certification, which is less burdensome than some feared. But the documentation and governance requirements are substantial.

The EU is effectively treating credit scoring AI with a level of regulatory scrutiny comparable to medical devices. For institutions operating across borders, this creates a compliance baseline that cannot be avoided.

ECB Supervisory Expectations: The 2025 Update

The European Central Bank's revised Guide to Internal Models introduced a dedicated section on machine learning, establishing that ML models used in banking must be adequately explainable and that model performance must justify the complexity introduced. The ECB defines machine learning as highly complex modelling techniques with many parameters, capable of capturing non-linearity.

The most consequential change is the extension of Model Risk Management expectations to all models, not just those used for regulatory capital calculations. This indicates that many banks were not validating their ML models with adequate rigour. The ECB's supervisory priorities for 2026 to 2028 confirm continued focus on banks' AI-related strategies, governance, and risk management, including whether institutions have appropriately skilled staff across model development, validation, use, and independent audit.

Federal Reserve SR 11-7 and Model Risk Management

The Federal Reserve's SR 11-7 guidance, issued in 2011, remains the foundational framework for model risk management in U.S. banking. It defines model risk as the potential for adverse consequences from decisions based on incorrect or misused model outputs. The guidance applies to all banking organisations supervised by the Federal Reserve, scaled to size and complexity.

SR 11-7 requires robust model development, effective validation, and sound governance. While it predates the current wave of AI adoption, its principles apply directly: effective validation requires understanding model outputs, which in turn requires explainability. The 2021 extension through SR 21-8, which applied model risk management principles to anti-money laundering and Bank Secrecy Act compliance systems, confirmed that these principles are technology-agnostic.

Basel Committee: The International Perspective

The Basel Committee on Banking Supervision has identified three focus areas for AI in banking: explainability, governance, and financial stability. The Committee's chair has warned that flaws in AI models could amplify instability in financial markets, noting that models relying heavily on historical patterns may fail to capture human behaviour during financial stress.

The Basel perspective adds an important dimension: systemic risk. Individual credit models that cannot be explained are not just institutional liabilities. When aggregated across the banking sector, unexplainable models that fail simultaneously could create systemic consequences. This concern elevates explainability from a compliance requirement to a financial stability imperative.

Regulatory Requirements at a Glance

| Framework | Jurisdiction | Explainability Requirement | Enforcement Status |

| FCRA / ECOA | United States | Specific reasons for adverse action; technology complexity is not an excuse | Active enforcement; $70M Apple Card fines (2024), $2.5M MA settlement (2025) |

| EU AI Act | European Union | High-risk classification for credit scoring; mandatory documentation and human oversight | Phased enforcement from 2024; high-risk requirements active |

| ECB Guide | Eurozone | ML models must be adequately explainable; MRM for all models | Supervisory priority 2026-2028; updated guidance July 2025 |

| SR 11-7 | United States | Model validation requires understanding outputs; governance scaled to complexity | Active since 2011; extended via SR 21-8 (2021) |

| Basel Committee | International | Explainability, governance, financial stability as focus areas | Ongoing guidance; chair warnings on systemic risk |

The Technical Solution: How Banks Are Implementing Explainability

The technical challenge of explaining credit decisions is real, but it is solved. Multiple methods exist, ranging from post-hoc explanation layers applied to black-box models to inherently interpretable architectures that require no additional explanation. The question for banks is not whether technical solutions are available. It is which approach fits their specific risk profile, regulatory obligations, and operational maturity.

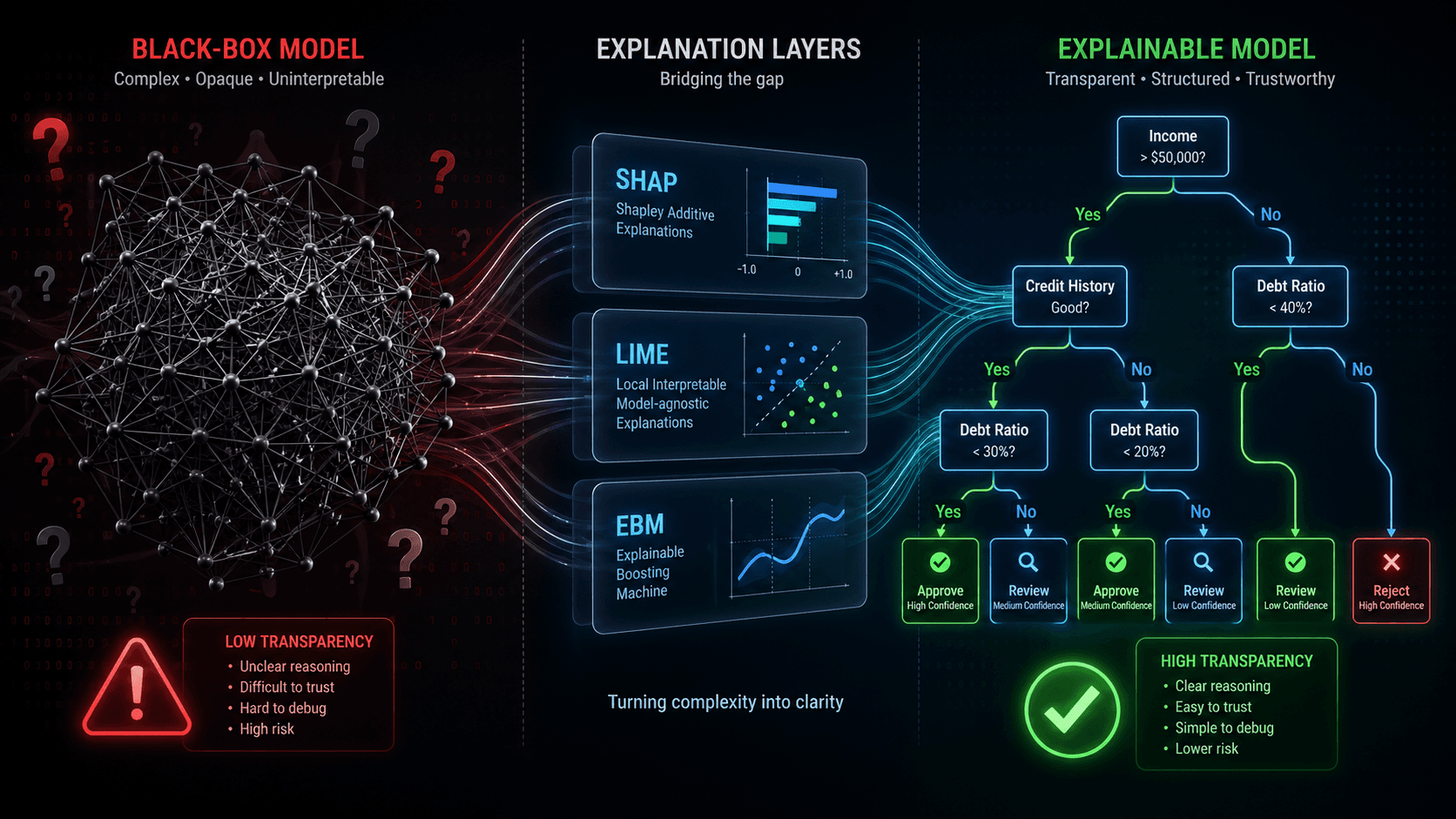

Post-Hoc Explanation Methods

SHAP (SHapley Additive exPlanations) uses game theory to determine each feature's contribution to a prediction. It provides both global explanations, showing which features matter most across the entire model, and local explanations, showing why a specific applicant received a specific decision. In credit risk, SHAP can generate the reason codes required for adverse action notices: it can explain that an applicant was denied primarily because of high credit utilisation and short credit history, with quantifiable importance scores for each factor.

Research from Norwegian banks using LightGBM with SHAP has demonstrated practical implementations where gradient boosting models achieve strong default prediction accuracy while SHAP provides the interpretability layer for regulatory compliance. The limitation is computational cost: SHAP calculations for complex models can be expensive, particularly when high-dimensional sampling is required.

LIME (Local Interpretable Model-Agnostic Explanations) takes a different approach. Rather than decomposing global model behaviour, LIME creates a simplified local model around each individual prediction. It generates synthetic data points similar to the instance being explained, then trains an interpretable model on those points. For credit decisions, this means LIME can explain individual approvals or denials in simple terms without requiring access to the full model architecture.

LIME's advantage is computational efficiency and the simplicity of its explanations, making it particularly useful for generating consumer-facing reason codes. Its limitation is that local explanations may not reflect global model behaviour, which can create inconsistencies when auditors compare explanations across decisions.

Counterfactual explanations show what would change a decision. Rather than explaining why an applicant was denied, a counterfactual states: if your income were $5,000 higher, the model would have approved the application. This approach satisfies the recourse requirement that regulators increasingly expect: rejected applicants should understand not just why they were denied but what they could change to receive a different outcome.

Inherently Interpretable Models

The more fundamental shift in credit risk modelling is the movement from explaining black boxes after the fact to building models that are transparent by design. As we analysed in our comparison of interpretable versus black-box models, this shift challenges the long-held assumption that accuracy requires complexity.

Explainable Boosting Machines (EBMs) represent the most significant development in this space. EBMs are tree-based cyclic gradient boosting models with automatic interaction detection. They combine the accuracy of gradient boosting with the transparency of interpretable models. The performance data is striking: an optimised EBM achieved a ROC-AUC of 0.983 on credit fraud detection, surpassing the XGBoost baseline of 0.975 and dramatically exceeding logistic regression at 0.948.

This matters because it undermines the foundational argument for black boxes in credit risk. If an inherently interpretable model matches or exceeds the accuracy of a black-box model, the case for opacity collapses. There is no accuracy sacrifice to justify, no trade-off to defend to regulators.

Cynthia Rudin's research at Duke University has been pivotal in establishing this point. Rudin and her team entered the Explainable Machine Learning Challenge, sponsored by FICO, Google, MIT, Oxford, and Berkeley, with the task of predicting loan default. The challenge organisers assumed that interpretable models could not compete with deep learning. Rudin's interpretable models achieved accuracy equal to the deep learning submissions while remaining simple enough to fit on an index card. Her broader research position, validated across criminal recidivism, medical diagnosis, and credit scoring, is that she has yet to encounter a problem where accuracy must be sacrificed for interpretability.

Logistic regression scorecards remain the historical standard in credit risk, with direct feature coefficients showing the direction and magnitude of each variable's impact. Regulatory acceptance is extremely high because the method has been used for decades. The limitation is real but narrowing: traditional logistic regression underperforms gradient boosting on complex datasets, with a measured gap of approximately 5.2 percentage points in AUC on Korean credit market data (0.906 versus 0.958). However, regularised logistic regression and hybrid approaches that use complex models for feature engineering and interpretable models for final decisions are closing this gap.

Model Performance Comparison

| Model | ROC-AUC | Interpretability | Regulatory Acceptance |

| Logistic Regression | 0.906 - 0.948 | Full: direct feature coefficients | Very high: decades of regulatory use |

| Explainable Boosting Machine (EBM) | 0.983 | Full: inherently interpretable | Growing: newer technique, strong evidence |

| XGBoost / LightGBM | 0.958 - 0.975 | Low: requires post-hoc explanation | Conditional: requires SHAP or LIME layer |

| Deep Neural Networks | ~0.975 | Very low: inherently opaque | Low: difficult to validate and audit |

Sources: Springer Nature systematic review; MDPI XAI credit risk study; Rudin FICO competition results

The Governance Challenge: Making Explainability Stick

Technical explainability solves the engineering problem. It does not solve the organisational one. The real challenge for most banks is not building an explainable model. It is ensuring that explainable models are properly developed, validated, monitored, documented, and governed across their entire lifecycle. This is where the gap between regulatory expectation and current practice is widest.

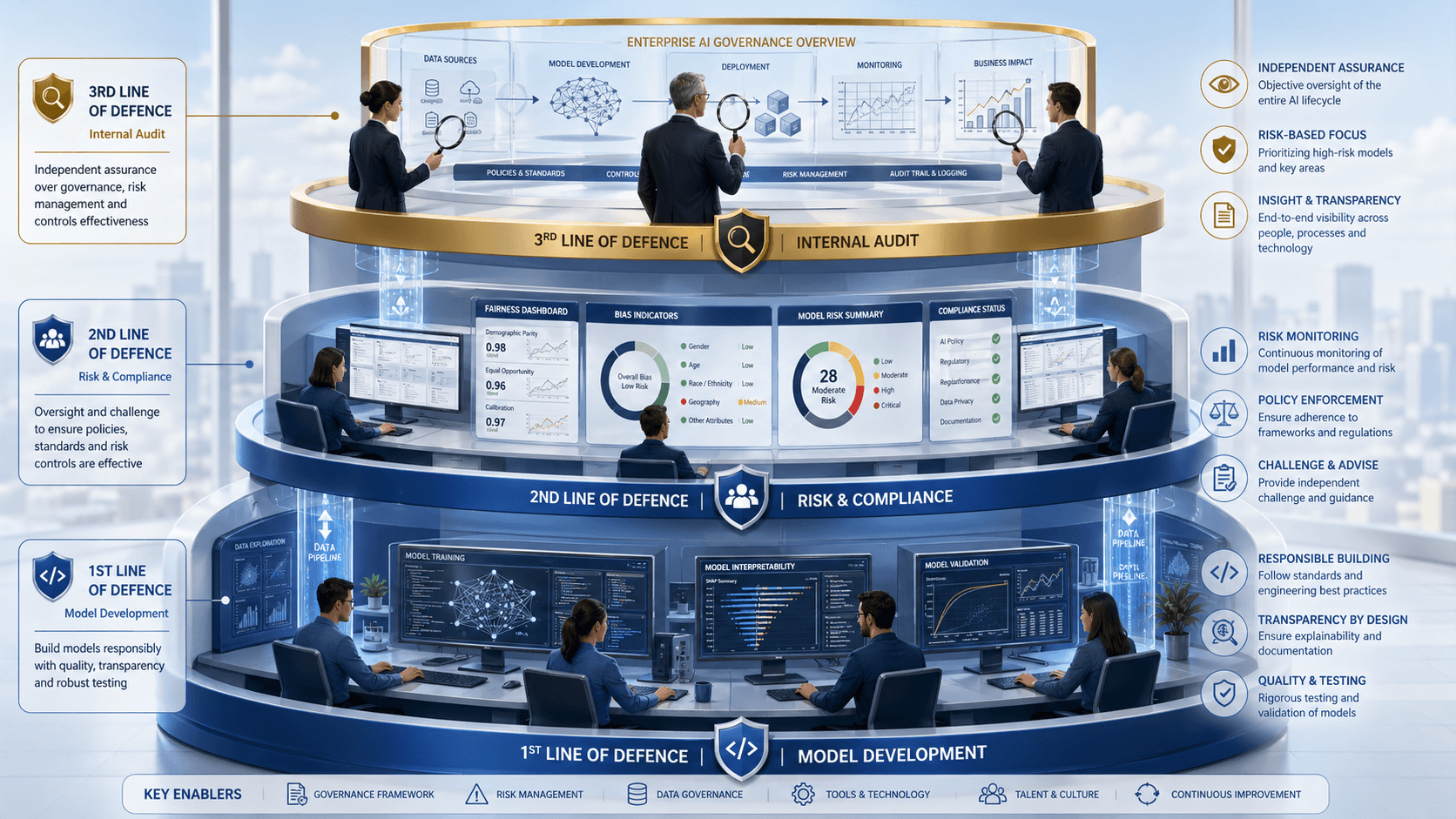

The Three Lines of Defence Applied to AI

Banking has long operated on a three-lines-of-defence model for risk management, and AI governance fits this structure naturally, if imperfectly.

The first line is the model development and operational teams who build and use credit models daily. They are responsible for appropriate model development, testing, and implementation. The challenge is that many model developers are trained in accuracy optimisation but not in explainability requirements. Building a model that passes a ROC-AUC threshold is a different skill from building one that can generate meaningful adverse action notices.

The second line is risk management and compliance, which provides oversight, sets rules, and monitors adherence. For AI credit models, this means reviewing model documentation, challenging first-line assumptions, and ensuring regulatory changes are reflected in governance frameworks. The challenge is that effective second-line oversight of machine learning models requires technical understanding that many compliance professionals do not yet have.

The third line is internal audit, which provides independent assurance that the first and second lines are operating effectively. Audit teams must objectively evaluate whether governance processes are working as designed and report findings to the board and audit committee. Here, the challenge is similar: auditing an AI model requires expertise that traditional audit teams are still developing.

The ECB's 2025 update extending Model Risk Management to all models signals recognition that many banks were not validating their ML models with adequate rigour. The governance gap is not theoretical. It is the gap that allowed Apple Card's algorithms to operate without anyone being able to explain their decisions.

Model Validation: Beyond Accuracy

Effective model validation in credit risk has traditionally focused on three components: conceptual soundness, outcome analysis, and ongoing monitoring. The challenge of AI is that each component now requires an explainability dimension that most validation frameworks were not designed to accommodate.

Conceptual soundness evaluation must now assess whether the model's design enables adequate explanation. Are the features interpretable? Can the model decompose its outputs into factors that satisfy adverse action notice requirements? If the model relies on hundreds of features with complex interactions, can the resulting explanations be validated by someone who is not a machine learning specialist?

Outcome analysis must extend beyond backtesting and stress testing to include fairness and bias testing. The Massachusetts settlement established that failing to test AI models for disparate impact is itself a violation. Quantitative fair lending analysis, covering approval rates by protected class, loan terms by demographics, and ongoing trend analysis, is now an explicit regulatory expectation.

Ongoing monitoring must track not just model accuracy over time but drift in explainability quality and emerging bias. A model that performed fairly at deployment can develop disparate impact as the population it serves changes. Continuous monitoring systems that detect performance degradation and bias emergence are becoming essential rather than aspirational.

The Documentation Gap

The ECB expects comprehensive documentation covering model architecture, data lineage, validation results, monitoring protocols, remediation procedures, and version control. In practice, many banks lack this level of documentation for their credit models. Regulatory reviews are increasingly identifying documentation gaps as material findings.

This is not a technical limitation. It is a governance maturity issue. Institutions that invested in documentation infrastructure early, treating model registries and validation records as first-class governance artefacts rather than afterthoughts, are finding that regulatory interactions proceed more smoothly and model updates can be deployed with lower risk.

As we examined in our analysis of Industry 5.0's principles, the human-centricity pillar is not just about consumer experience. It extends to the organisational capacity to govern the systems that serve consumers. A bank that deploys a model it cannot document has not achieved human-centric AI in any meaningful sense.

The Business Case: Why Compliance Is Also Competitive Advantage

The framing of explainability as regulatory burden misses the economics. Banks that have invested in explainable AI systems are not just avoiding fines. They are operating more efficiently, deploying models faster, and building customer trust that translates into measurable commercial outcomes.

The Economics of AI in Credit

The adoption data tells a compelling story. Over 70 percent of top-tier U.S. banks now use AI for loan underwriting. Three-quarters of banks globally are using machine learning for credit scoring, early warnings, and pricing. AI-enhanced credit scoring models have increased loan approval rates for underbanked individuals by 22 percent while simultaneously reducing default rates by 18 percent. Leading platforms have reduced end-to-end origination time from three to five days to under sixty minutes, with per-loan processing cost reductions of 30 to 40 percent.

Institutions that have not deployed production-grade AI models by the end of 2026 face a projected 15 to 20 percent cost disadvantage in consumer lending versus AI-native competitors. This creates a dual imperative: banks must adopt AI for competitive reasons, but they must adopt it with explainability built in for regulatory reasons. The institutions that treat these as the same project rather than competing priorities are the ones moving fastest.

The Cost of Getting It Wrong

The enforcement precedent is now quantifiable. Apple Card's $70 million in combined fines, the Massachusetts settlement's $2.5 million plus mandated governance overhaul, and the CFPB's explicit guidance that technology complexity is not a defence have established a clear cost baseline for non-compliance.

The non-financial costs may be even more significant. Reputational damage from being associated with algorithmic discrimination is difficult to quantify but impossible to ignore. The Apple Card investigation generated international media coverage and became a case study in business schools within months. Management distraction from multi-year regulatory investigations, investor concerns about governance red flags, and the challenge of recruiting talent to an institution known for discriminatory outcomes all compound the direct financial penalties.

Consumer Trust as Differentiator

Survey data from 2025 shows that consumer attitudes toward AI in financial services are nuanced. Sixty-four percent of consumers are comfortable with AI being used in credit calculations, but only 39 percent trust AI for autonomous financial planning decisions. Forty-eight percent prioritise transparency in how decisions are made, and 46 percent require human oversight to be available. Fifty-seven percent rank data security as their top concern.

These numbers represent both a challenge and an opportunity. Banks that can communicate how their credit decisions are made, that can tell an applicant exactly which factors influenced their outcome and what they could change to receive a different result, are meeting a demonstrated consumer demand. In a market where product differentiation in lending is increasingly difficult, the ability to say 'we can explain every decision' is a positioning advantage that compounds over time.

As we explored in our guide to data-driven decisions, the quality of decisions depends not just on the data and models involved but on the governance and transparency surrounding the entire decision process.

What Comes Next: The Direction of Travel

The regulatory framework for AI in credit risk is still hardening, but the direction is unmistakable. Several trends will shape the next two to three years.

From Post-Hoc to Inherently Interpretable

The period from 2023 to 2024 was defined by SHAP and LIME as the primary solutions for AI explainability in credit: take a black-box model, add an explanation layer, and present the results to regulators. The period from 2025 to 2026 is seeing a shift toward inherently interpretable models, particularly EBMs and regularised logistic regression variants. By 2027 to 2028, expect regulatory preference to solidify around models that are interpretable by design rather than explained after the fact.

This shift reflects a recognition that post-hoc explanation layers add complexity and may not accurately reflect full model behaviour. A SHAP explanation of a neural network's credit decision is an approximation, not a guarantee. An EBM's decision is transparent by construction. For regulators concerned with auditability and consistency, the inherently interpretable approach offers stronger assurances.

Governance Frameworks Formalising

The ECB's extension of Model Risk Management to all models, Basel's continued focus on explainability and governance, and the CFPB's enforcement trajectory all point toward formal, codified standards for ML governance in banking. Expect 2026 and 2027 to bring specific guidelines for machine learning model validation, formalised bias testing requirements, monitoring and drift detection expectations, and defined skill requirements for model validators.

Institutions that invest in governance infrastructure now are building the institutional knowledge and processes that will become regulatory requirements later. This is the pattern we examined in our analysis of the EU AI Act's broader implications: early movers who treat compliance as strategic investment gain advantages that late movers cannot easily replicate.

Emerging Risks Still Unaddressed

Several challenges remain at the frontier. Model drift, the gradual degradation of model performance over time, lacks clear regulatory guidance on revalidation frequency and acceptable thresholds. Data poisoning, where training data is contaminated or manipulated, represents a security concern that explainability alone does not address. Adversarial attacks against credit models, interconnected risk when credit decisions cascade through financial systems, and emerging biases in new subpopulations all represent areas where regulatory guidance is likely but not yet formalised.

These represent the next generation of challenges for credit risk AI. The institutions that start addressing them now, rather than waiting for regulatory mandates, will be better positioned for the regulatory environment of 2028 and beyond.

Conclusion: Explainability Is the Foundation, Not the Ceiling

The convergence of regulatory enforcement, technical capability, and consumer expectation has made explainability in credit risk non-negotiable. The Apple Card investigation and the Massachusetts settlement are not outliers. They are the beginning of a sustained enforcement pattern that will only intensify as the EU AI Act's requirements take full effect and supervisory bodies refine their expectations for machine learning governance.

The technical solutions exist. EBMs demonstrate that interpretable models can match or exceed black-box accuracy. SHAP and LIME provide explanation layers for institutions that have already deployed complex models. Counterfactual explanations offer consumers the recourse information that regulators increasingly expect. The accuracy-versus-interpretability trade-off, long used to justify black-box models in credit risk, is a myth that empirical evidence has debunked.

The harder challenge is governance: building the organisational capacity to develop, validate, monitor, and document AI credit models across their full lifecycle. This requires investment in people, processes, and infrastructure that extends well beyond the data science team. It requires risk professionals who understand machine learning, auditors who can evaluate model behaviour, and leadership that views explainability as strategic advantage rather than compliance cost.

Banks that build this capacity now are not just meeting today's regulatory requirements. They are positioning themselves for faster model deployment, lower compliance costs, stronger customer trust, and reduced risk of the enforcement actions that are increasingly defining the competitive landscape. The institutions that treat transparency as a built-in design principle rather than a regulatory afterthought will lead the next era of credit risk management.

For those building careers in this space, as we explored in our guide to data-related career paths, the convergence of machine learning, regulation, and governance is creating demand for professionals who can bridge technical and compliance domains. Explainability is not just a model requirement. It is a professional skill set that will define the most valuable roles in financial services AI for years to come.