Imagine applying for a mortgage and being declined. You ask why. The bank tells you: "The model said no." No reason, no breakdown, no path forward. That is the reality of unexplainable AI, and it is already shaping decisions about credit, insurance, hiring, and medical treatment across the world.

Explainable AI (XAI) is the practice of building machine learning systems whose decisions humans can understand, audit, and trust. It is not an academic luxury or an optional feature. In 2026, it is a regulatory requirement, a business necessity, and, increasingly, an ethical imperative.

Organisations spent over $37 billion on enterprise AI in 2025, yet only 20% successfully deployed AI into production. The most common bottleneck? Stakeholders could not understand what the models were doing or why. That gap between capability and trust is exactly what explainable AI exists to close.

What You Will Learn in This Post

· What explainable AI actually means, beyond the textbook definition

· Why the EU AI Act, Basel framework, and GDPR all demand transparency from AI systems

· The real difference between interpretable models and post-hoc explainability methods like SHAP

· How unexplainable AI has caused harm in healthcare and financial services

· Why the "accuracy versus interpretability" trade-off is often a myth

What Is Explainable AI?

At its core, explainable AI refers to techniques and design choices that make it possible for humans to understand how a machine learning model arrives at a specific output. The goal is not to simplify the model itself, but to provide a clear, trustworthy account of the reasoning behind each prediction.

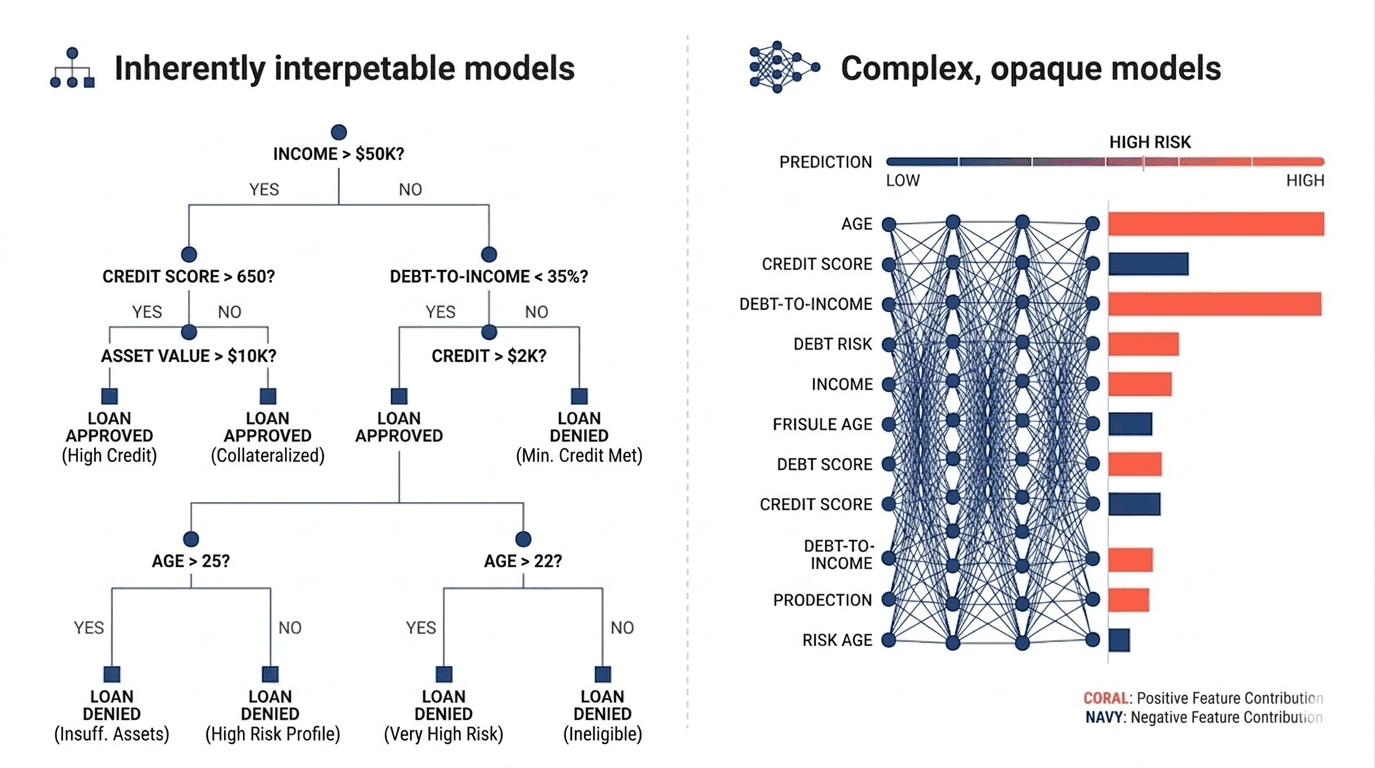

There are two broad approaches. The first uses inherently interpretable models: algorithms like logistic regression, decision trees, scorecards, and generalised additive models (GAMs) whose internal mechanics are transparent by design. If you have explored how machine learning and analytics are shaping finance, you will recognise these as the backbone of credit risk modelling in regulated banking.

The second approach uses post-hoc explainability methods: tools applied after training to interpret a complex model. SHAP (SHapley Additive exPlanations) and LIME (Local Interpretable Model-agnostic Explanations) are the most widely adopted. According to a BIS paper on AI explainability for financial regulators, feature importance and SHAP are the two most commonly used explainability techniques among UK financial institutions.

The distinction matters. An inherently interpretable model can explain itself. A post-hoc method offers an approximation of why a complex model behaved the way it did. Both have their place, but understanding the difference is essential before choosing an approach for high-stakes applications.

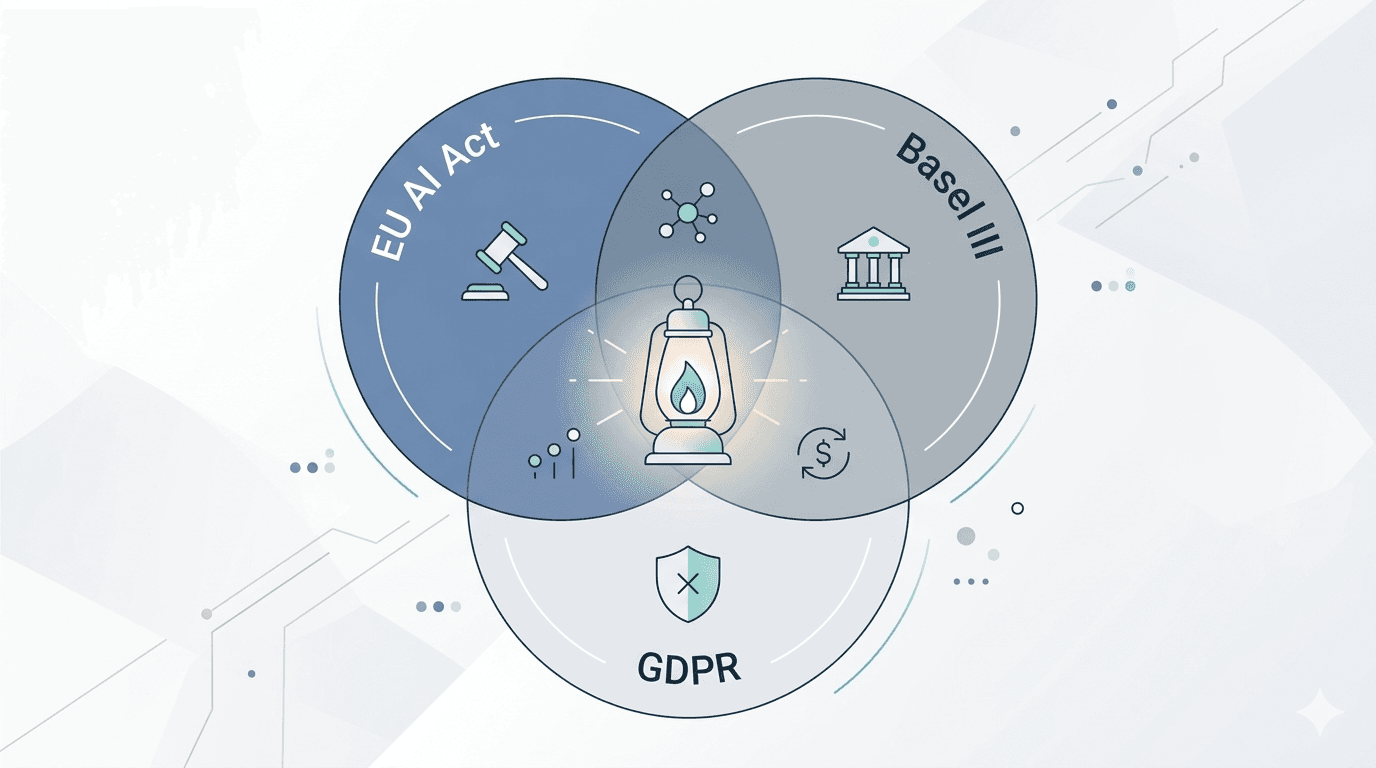

The Regulatory Case: Why Governments Demand Transparency

The EU AI Act

The EU AI Act, which enters its enforcement phase in August 2026, classifies AI systems by risk tier. High-risk systems, including those used in credit scoring, employment decisions, and essential public services, must be "sufficiently transparent to enable deployers to interpret a system's output." Non-compliance carries penalties of up to 35 million euros or 7% of global turnover.

This is not abstract policy. If your organisation deploys a credit-scoring model in the EU and cannot explain its decisions to a regulator, you are exposed to significant financial and legal risk. As we explored in the NeuroNomixer manifesto, the gap between AI capability and AI governance is one of the defining challenges of this decade.

Basel III and Banking Regulation

Financial regulators have demanded model transparency long before the AI Act. The Basel Committee on Banking Supervision has emphasised since the introduction of internal models that a "black box" not well understood by bank personnel does not provide confidence in the rating process. Basel III introduced input and output floors partly to temper reliance on opaque internal models.

For banks and financial institutions, explainability is not a new concern. It is a long-standing regulatory expectation that AI has made more urgent, not less.

GDPR and the Right to Explanation

The General Data Protection Regulation grants individuals the right not to be subject to decisions based solely on automated processing that significantly affect them. While legal scholars debate the exact scope of GDPR's "right to explanation," the practical reality is clear: organisations using AI to make consequential decisions about people must be prepared to explain how those decisions were made. Understanding what constitutes personal data under GDPR is a critical first step.

When AI Cannot Explain Itself: Real-World Consequences

Healthcare: The Optum Algorithm

One of the most widely cited examples of AI harm involved an algorithm used by US health insurers to identify patients who needed extra care. The system predicted healthcare costs as a proxy for illness severity. Because Black patients historically had less money spent on their care (due to systemic inequities in access), the model systematically underestimated their needs. The result: Black patients were far less likely to be flagged for high-risk care management than equally sick white patients.

Had the model been explainable, and had its developers examined which features were driving predictions, this bias could have been detected before deployment. Explainability is not just about compliance; it is about catching harm before it reaches real people.

Banking: The Black-Box Credit Decision

Consider a bank that deploys a gradient-boosted ensemble model for credit decisions. The model performs well on accuracy metrics. But when a customer challenges a declined application, the bank cannot produce a clear explanation. The regulator asks for documentation of the decision logic. The compliance team cannot provide it.

This scenario is not hypothetical. It is the reason why model validation teams in banks routinely reject black-box models regardless of their accuracy. As the CFA Institute has documented, SHAP-based explanations can bridge the gap between ensemble model performance and regulatory acceptance under Basel III and GDPR, but only when explainability is built into the workflow from the start.

The Accuracy Versus Interpretability Myth

A common assumption in machine learning is that there is an unavoidable trade-off: more complex models are more accurate, and simpler models sacrifice performance for transparency. This framing has shaped how many teams approach model selection, defaulting to deep learning or large ensembles "just in case" the accuracy gain matters.

Recent research challenges this assumption directly. A study published in the Harvard Data Science Review examined high-stakes machine learning applications across healthcare, criminal justice, and other domains. The finding: in many cases, black-box models offered no meaningful accuracy advantage over inherently interpretable alternatives.

This matters enormously for practitioners in data-driven decision-making. If a logistic regression or a scorecard delivers comparable predictive performance to a neural network, and you can explain every decision it makes, the case for the black box evaporates. The trade-off is not accuracy versus interpretability. It is often unnecessary complexity versus clarity.

This does not mean complex models are never appropriate. In low-stakes applications, in scenarios with enormous feature spaces, or in domains where the cost of a wrong prediction is low, neural networks and ensemble methods earn their place. But in regulated, high-stakes environments like banking, insurance, and healthcare, the burden of proof falls on the black box to justify its opacity.

Making Explainability Work in Practice

Explainability is not something you bolt on at the end of a project. It must be embedded in the design from the beginning. Here is how organisations are approaching this in practice.

Start With the Right Model

Before reaching for a complex algorithm, ask whether a simpler, inherently interpretable model meets the performance requirements. Scorecards, logistic regression, and GAMs remain the workhorses of credit risk modelling for good reason: they are transparent, auditable, and well understood by regulators. As explored in our coverage of machine learning in finance, Explainable Boosting Machines (EBMs) offer a middle ground, combining ensemble-level performance with additive model interpretability.

Use Post-Hoc Methods When Complexity Is Justified

When a complex model is genuinely necessary, SHAP and LIME provide the tools to explain its behaviour. SHAP assigns each feature a contribution score for a given prediction, grounded in cooperative game theory. LIME generates a local approximation of the model around a single prediction point. Both have limitations: SHAP can be computationally expensive on large datasets, and LIME's local explanations may not generalise. But used thoughtfully, they transform opaque predictions into actionable explanations.

Document Everything

Regulatory frameworks like the EU AI Act and Basel III do not just require that models be explainable. They require that the explanation be documented, reproducible, and available for audit. This means logging feature contributions, maintaining model cards, and establishing clear governance around who reviews and approves model outputs. Understanding the data ecosystem that feeds these models is a prerequisite for meaningful documentation.

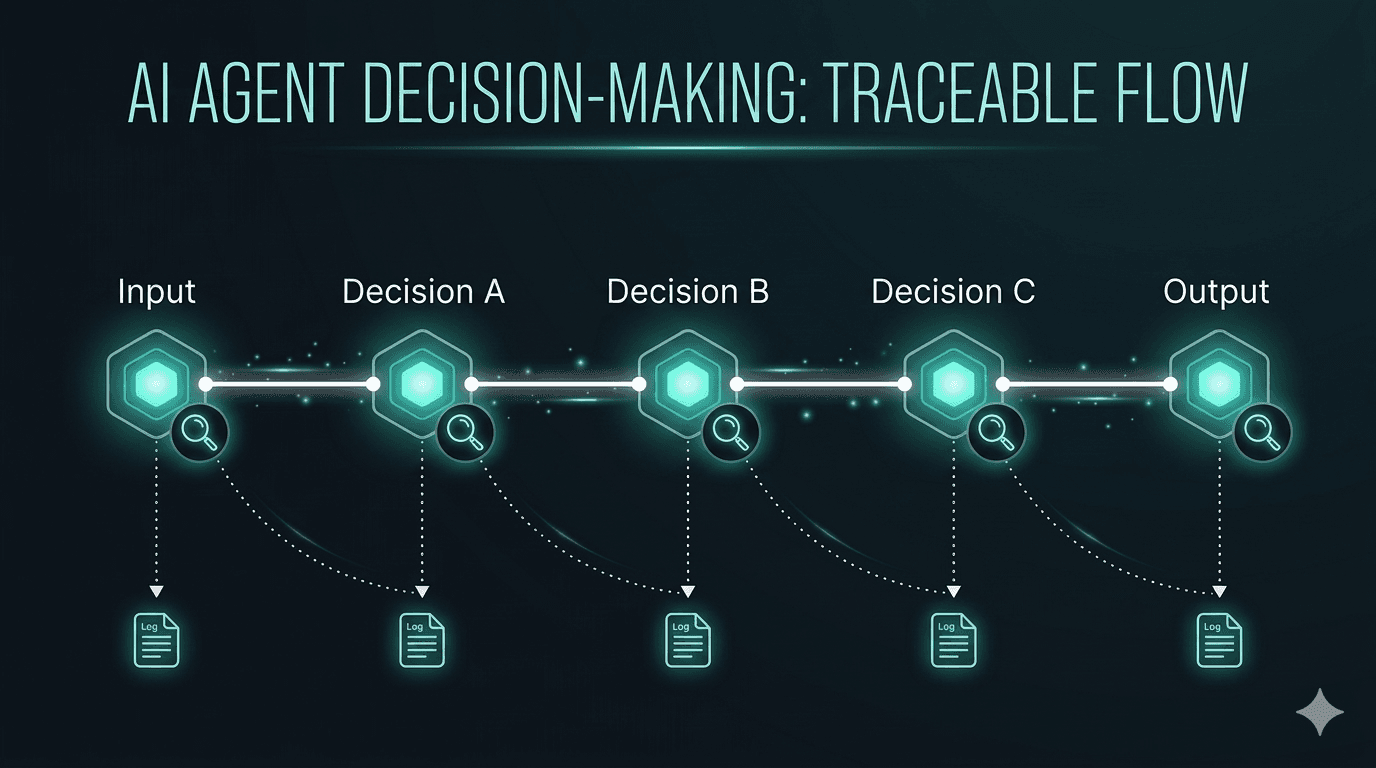

The Road Ahead: Agentic AI and the Next Explainability Challenge

The explainability challenge is evolving. As AI moves from standalone prediction models to agentic systems that make chains of autonomous decisions, the question is no longer "why did the model predict X?" but "why did the agent take actions A, B, and C in sequence?" Traceable decision chains are becoming the new frontier of AI transparency.

For professionals building careers in data and analytics, explainability is no longer a niche specialism. It is a core competency. Whether you work in model development, risk management, compliance, or product design, your ability to explain and audit AI decisions will define your value in the years ahead.

Conclusion: Explainability Is Not Optional

Explainable AI is not a constraint on innovation. It is a foundation for responsible innovation. The organisations that treat transparency as a design principle, rather than a compliance checkbox, will build systems that earn trust from regulators, customers, and the public.

The EU AI Act sets the regulatory floor. The Basel framework and GDPR reinforce it. But the real argument for explainability goes beyond avoiding penalties: it is about building AI systems that work for people, not just on them.

In an upcoming post, we will go deeper into the practical trade-offs between interpretable and black-box models, examining when complexity is justified and when simplicity wins. Stay tuned.

Continue Reading

· Exploring How Machine Learning and Analytics Shape the Future

· What NeuroNomixer Stands For: AI, Data, and the Future of Systems