On January 8, 2026, the European Commission ordered X to retain all data related to its AI chatbot Grok. In July 2025, Meta publicly refused to sign the EU's Code of Practice for general-purpose AI, calling it regulatory overreach. In December 2024, Italy's data protection authority fined OpenAI €15 million for GDPR violations related to ChatGPT. These are not theoretical policy debates. They are enforcement actions with real financial consequences, happening right now.

By August 2, 2026, the EU AI Act's rules for high-risk AI systems take full effect. This date is to AI regulation what May 25, 2018 was to data privacy: the moment compliance shifts from optional to mandatory, and the penalties for getting it wrong become severe. Companies deploying AI in recruitment, credit scoring, fraud detection, biometric identification, and dozens of other domains must have risk management systems, technical documentation, human oversight mechanisms, and ongoing monitoring in place. Non-compliance carries fines of up to €35 million or 7 percent of global turnover.

But this is not just a European story. The world is splitting into three distinct AI governance models: the EU's precautionary approach, the United States' competitive fragmentation, and the United Kingdom's flexible middle ground. Each model reflects different values, different risk tolerances, and different bets on what drives innovation. The choices made in the next eighteen months will shape the global AI industry for a decade.

As we explored in our detailed analysis of the EU AI Act's requirements, the Act is the most comprehensive AI legislation in the world. This post examines something broader: how AI governance as a whole, not just one regulation, is actively reshaping how technology companies build, deploy, and market their products across Europe and beyond.

What You Will Learn in This Post

• How the EU AI Act is being enforced right now, who has been fined, and what the August 2, 2026 deadline means for every company deploying AI in Europe

• The three competing regulatory models (EU, US, UK) and how each is betting on different trade-offs between safety and speed

• Whether regulation is actually stifling European innovation, with real investment data, startup formation rates, and the nuances that most coverage misses

• How major tech companies (Google, Meta, Microsoft, Amazon, Mistral AI) are responding: adaptation, confrontation, and strategic positioning

• The Brussels Effect: whether EU rules are becoming the global default, and the three factors limiting that influence

• What comes next in 2026 and 2027, including the Digital Omnibus proposal that could reshape the entire timeline

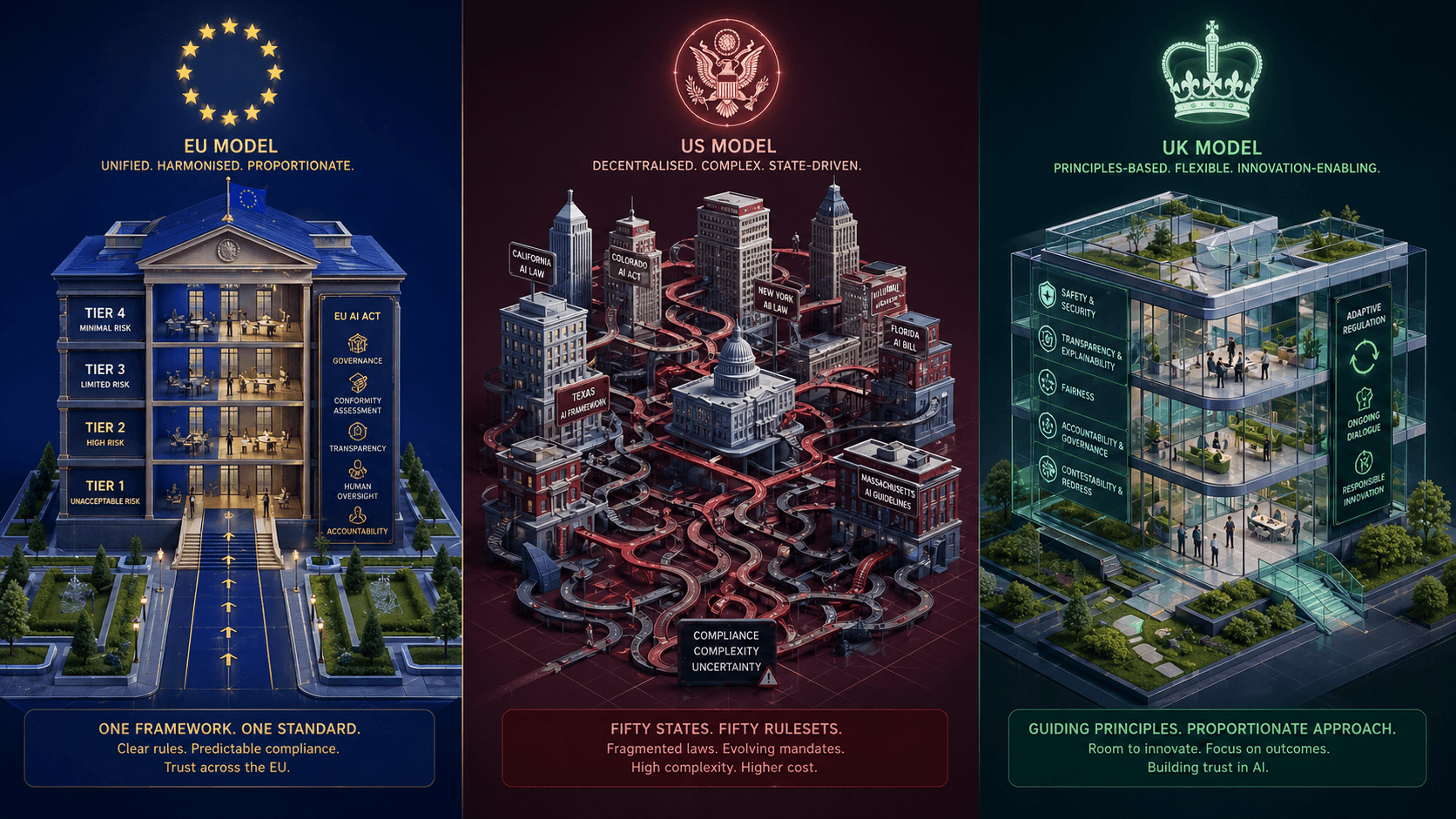

Three Regulatory Models, Three Futures

The global AI governance landscape is not converging. It is diverging into three distinct models, and companies operating internationally must navigate all of them simultaneously.

The EU: Precautionary and Rights-Based

The EU AI Act establishes a risk-based framework that classifies AI systems into four tiers: unacceptable risk (banned outright), high risk (subject to extensive compliance requirements), limited risk (transparency obligations), and minimal risk (largely unregulated). Credit scoring, recruitment, fraud detection, and biometric identification all fall into the high-risk category under Annex III.

The compliance costs are real. Industry estimates put the annual cost at approximately €29,277 per AI unit in production, with certification costs of €16,800 to €23,000 per unit. For large technology companies, these costs are absorbable. For startups and SMEs, they can represent a significant barrier. Over 33 percent of EU AI startups could see their products classified as high-risk, triggering the full compliance regime.

The EU's bet is that setting high standards early will build consumer trust, create competitive advantages for compliant companies, and establish European values as the global baseline. Whether that bet pays off depends on implementation, enforcement, and whether the costs drive innovation elsewhere.

The United States: Competitive Fragmentation

The US has taken a deliberately different path. A December 2025 executive order established a federal policy framework that prioritises American AI leadership over precautionary regulation. The order created a task force to challenge state AI laws on constitutional grounds and directed the Secretary of Commerce to evaluate state laws that conflict with federal policy within 90 days.

The result is regulatory fragmentation. California's Transparency in Frontier AI Act took effect in January 2026. Colorado's AI Act is scheduled for June 2026. Other states are developing their own approaches. Federal preemption is being pursued aggressively, but the legal challenges will take years to resolve. For companies, this means navigating a patchwork of potentially conflicting requirements with no clear endpoint.

The United Kingdom: Flexible Middle Ground

The UK has positioned itself as a third option. Its pro-innovation approach, outlined in a 2023 white paper and reinforced through subsequent policy actions, relies on principles-based guidance rather than prescriptive rules. Existing sector regulators (the FCA for financial services, the ICO for data protection, Ofcom for communications) apply AI-relevant principles within their existing mandates.

The UK's proposed AI Growth Lab would create cross-economy sandboxes with targeted regulatory modifications, sending a clear message: it wants AI founders to build here. The rebranding of the AI Safety Institute to the AI Security Institute reflects a shift from precaution to competitive positioning. The UK is betting that flexibility and speed will attract the companies that find the EU too prescriptive and the US too fragmented.

Regulatory Framework Comparison

| Dimension | European Union | United States | United Kingdom |

| Approach | Risk-based, precautionary, fundamental rights focus | Fragmented; federal preemption vs state laws | Principles-based, sector-specific, pro-innovation |

| Primary legislation | EU AI Act (2024); fully enforceable Aug 2026 | No comprehensive federal law; state laws emerging | No dedicated AI Act; sector regulators apply existing powers |

| Enforcement | EU AI Office + national authorities; fines up to 7% turnover | FTC, state AGs; varying penalties | Sector regulators (FCA, ICO, Ofcom); proportionate enforcement |

| Innovation support | Regulatory sandboxes, AI Pact, €20B investment plan | Tax incentives, defence spending, minimal compliance burden | AI Growth Lab, sandboxes, reduced regulatory friction |

| Strategic bet | Trust and standards as competitive advantage | Speed and scale through deregulation | Flexibility attracts global talent and capital |

The August 2, 2026 Deadline: What Actually Changes

The EU AI Act's implementation timeline is phased, but August 2, 2026 represents the most significant enforcement milestone. This is when the rules for high-risk AI systems, the transparency obligations under Article 50, and the full enforcement powers of the AI Office all take effect simultaneously.

High-Risk AI Rules Go Live

Every AI system classified as high-risk under Annex III must have comprehensive risk management systems, high-quality data governance, technical documentation, human oversight mechanisms, logging capabilities, and continuous monitoring in place. The categories affected are extensive: AI used in recruitment and human resources, credit scoring and loan underwriting, fraud detection, biometric identification, critical infrastructure management, law enforcement, and education.

The penalty framework is designed to be deterrent. Violations of prohibited practices carry fines of up to €35 million or 7 percent of global annual turnover, whichever is higher. General violations carry fines of up to €15 million or 3 percent of turnover. For a company like Google (Alphabet revenue approximately $350 billion), the maximum fine for a prohibited practice would exceed $24 billion. These are not theoretical numbers. The enforcement mechanisms are now operational.

Transparency Obligations Begin

Article 50 requires that AI-generated content be marked as artificial, with machine-readable marking for deepfakes and synthetic media. The Code of Practice on transparency provides guidance on implementation, but the legal obligation is clear: content platforms, generative AI providers, and search engines must ensure users can distinguish AI-generated material from human-created content.

Regulatory Sandboxes Become Mandatory

Under Article 57, each EU member state must establish at least one AI regulatory sandbox by August 2, 2026. These controlled environments allow companies to test AI systems before full market release, with regulatory guidance and reduced compliance risk during the testing phase. Several member states have already launched or announced sandboxes, but the December 2025 consultation on implementation rules suggests the infrastructure is still being built.

The Omnibus Uncertainty

There is one significant complication. The Digital Omnibus proposal, introduced by the European Commission in November 2025, would push the high-risk AI enforcement deadline from August 2026 to December 2027, with regulated product rules delayed to August 2028. The proposal aims to simplify overlapping regulations across the AI Act, GDPR, Data Act, and DORA. It is currently in trilateral negotiations and could take months to finalise.

The practical advice for companies is to plan for August 2, 2026 unless and until the Omnibus formally passes. Organisations that delay compliance planning based on the assumption of a postponement are taking a calculated risk.

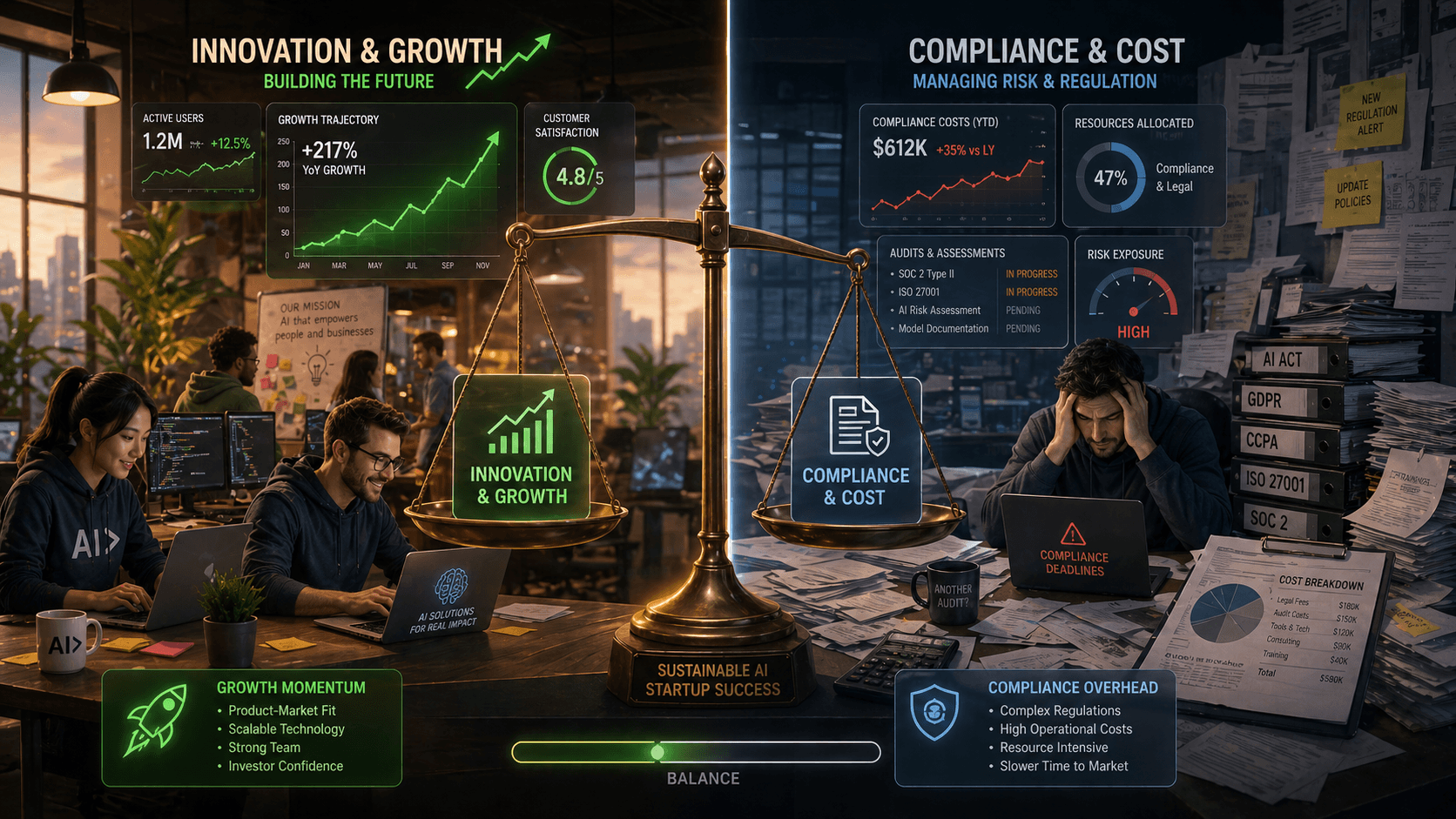

The Innovation Debate: What the Data Actually Shows

The question of whether EU AI regulation stifles or stimulates innovation generates more heat than light. The data tells a more nuanced story than either camp typically admits.

The Case That Regulation Is Hurting

The evidence for regulatory burden is real and measurable. Compliance costs of approximately €29,277 per AI unit annually represent a genuine expense, particularly for smaller companies. In July 2025, 56 European AI companies, including Mistral AI and Aleph Alpha, publicly urged the Commission to pause enforcement, arguing the rules were too burdensome for a sector still finding its footing.

The talent picture is concerning. Net tech talent inflow to the EU fell from approximately 52,000 in 2022 to 26,000 in 2024. While the EU has 30 percent more AI professionals per capita than the United States, better funding and clearer career paths in the US continue to attract European talent. Three of four European international AI PhD students at US universities stay for at least five years.

The startup funding gap compounds the issue. European AI startups raise approximately €8.5 million in their first funding round, compared to $13 million for US counterparts. At the growth stage, the EU invests roughly three times less than the US. At the late stage, the gap widens to nine times. A Harvard Kennedy School analysis found that a 200 percent increase in fixed compliance costs can flip a startup's margins from positive 13 percent to negative 7 percent.

The Case That Regulation Is Helping

The counter-evidence is equally compelling. EU AI investment jumped 75 percent year-over-year from approximately $10 billion in 2024 to $17.5 billion in 2025, with AI becoming the leading venture sector in Europe for the first time. Mistral AI raised $2 billion in the largest European AI funding round of 2025, its co-founder simultaneously signing a letter urging regulatory pause while successfully raising at scale.

The first harmonised standard for AI Act compliance (prEN 18286) entered public inquiry in October 2025, providing the legal certainty that companies need to plan compliance investments with confidence. Companies signing the GPAI Code of Practice, including Google, Amazon, Apple, and Microsoft, gain a presumption of conformity that reduces their legal risk. Over 130 companies have signed the AI Pact voluntary compliance commitments.

The EU has also committed significant public investment: a €20 billion AI Continent Action Plan announced in April 2025, plus an additional €1 billion under the Apply AI Strategy for sectoral adoption.

The Nuance That Matters

The honest assessment is that both narratives contain truth, and the impact depends heavily on company size, sector, and stage.

Large technology companies can absorb compliance costs and may even benefit from them as barriers to entry against smaller competitors. SMEs and early-stage startups face proportionally higher burdens, which is why the Omnibus proposal includes simplified quality management options for smaller companies.

More fundamentally, Europe's AI investment gap predates the AI Act. The structural issues, including less available late-stage capital, fewer large European acquirers, and a venture ecosystem that is decades younger than Silicon Valley's, existed before AI regulation entered the picture. Removing the AI Act entirely would not suddenly close the six-to-one funding gap with the United States.

As we examined in our analysis of Industry 5.0 and its human-centred principles, the question is not whether to regulate but how to regulate in ways that support both safety and growth. The EU's ongoing recalibration through the Omnibus proposal suggests Brussels recognises the balance needs adjustment.

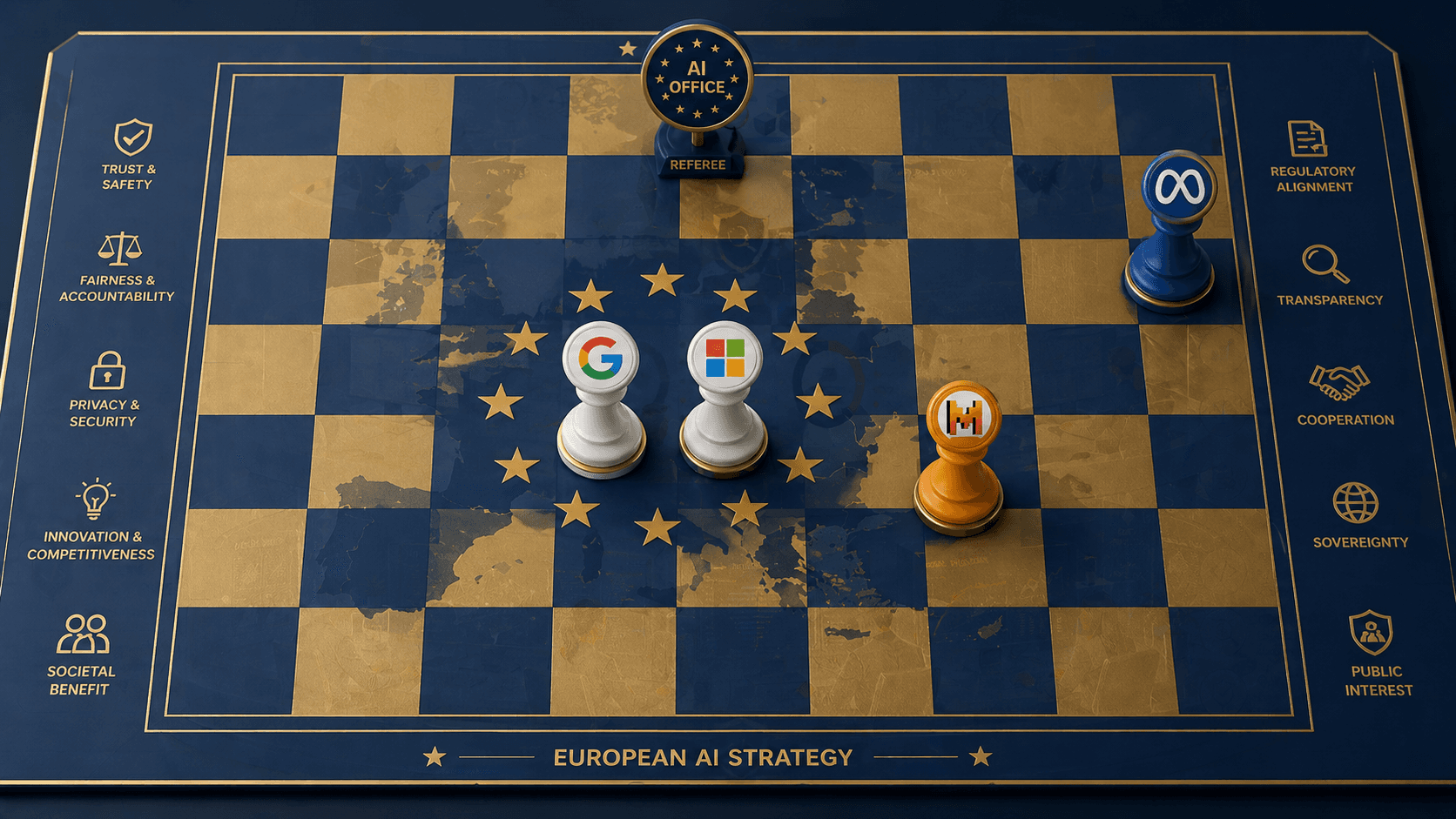

How Companies Are Responding: Adaptation Over Exodus

Contrary to early predictions, the major technology companies have not withdrawn AI products from the European market. Their responses range from full compliance to public confrontation, but the dominant pattern is strategic adaptation.

Google: Compliance as Strategy

Google signed the GPAI Code of Practice, integrated AI into core services including search overviews powered by Gemini, and is adapting transparency practices for Article 50 requirements. The company faces a December 2025 antitrust investigation regarding use of online content to train AI models, but its compliance posture positions it as a responsible actor in regulatory discussions. Google's approach treats compliance expertise as a competitive moat.

Microsoft: Governance-First Positioning

Microsoft signed the Code of Practice and established dedicated compliance working groups combining AI, legal, policy, and engineering teams. Its EU AI Act compliance page demonstrates a deliberate strategy of using regulatory leadership as brand differentiation. For enterprise customers evaluating AI vendors, Microsoft's compliance infrastructure is a selling point.

Meta: Confrontation and Risk

Meta's approach stands in sharp contrast. The company publicly refused to sign the GPAI Code of Practice in July 2025, with representatives telling CNBC that the Code exceeds the Act's legal scope and would stunt growth. Meta's Llama models remain available in Europe but under closer scrutiny from the AI Office. In January 2026, the Commission expanded its investigation into Meta's use of the WhatsApp Business API.

This confrontational strategy carries material risk. If enforcement tightens after August 2, 2026, Meta could face higher fines or more restricted operations than competitors who established compliance track records early.

Mistral AI: Rhetoric Versus Reality

Mistral AI offers perhaps the most instructive case. Its co-founder signed the July 2025 letter urging Brussels to pause enforcement, and the company has been vocal about regulatory burden. Yet it raised $2 billion in the same year, launched new products, and remains firmly EU-focused. The disconnect between rhetoric and behaviour suggests that regulation is a cost and complication but not the existential threat some portray it as.

What Is Not Happening

It is worth noting what the data does not show. There is no major exodus of AI products from the EU market. There is no emerging 'Europe AI-free zone.' Startup formation rates remain strong, with nearly 25 percent of European startups now AI-backed. The narrative of regulatory destruction does not match the observable evidence, even if the concerns about cost and complexity are legitimate.

The Brussels Effect: Real but Limited

The Brussels Effect, the phenomenon where EU regulations become de facto global standards, has been well documented for chemical safety, data privacy, and product standards. The question is whether it will apply to AI governance.

Where It Works

Large technology companies tend to apply EU standards globally rather than maintaining separate product versions per region. If you redesign your AI system to meet EU high-risk requirements, it is often more economical to deploy that version everywhere than to manage regulatory divergence. Google, Microsoft, and Amazon, all GPAI Code signatories, are likely applying at least some EU-driven standards across their global operations.

The Brookings Institution analysis acknowledges this de facto influence while noting important limitations. The GovAI research at Oxford found that the EU's regulatory influence on AI is real but conditional: it depends on enforcement credibility, market size, and whether alternative regulatory models offer companies a viable escape route.

Where It Breaks Down

Three factors limit the Brussels Effect for AI. First, the United States is explicitly rejecting convergence: the December 2025 executive order's federal preemption strategy is designed to prevent EU-style regulation from taking hold domestically. Second, China is developing its own governance model focused on content control and state priorities, bearing little resemblance to the EU's rights-based framework. Third, the UK is positioning itself as an alternative for companies that want a lighter regulatory touch.

The implication for companies is that a single global compliance strategy is becoming less viable, not more. Regulatory divergence across the EU, US, UK, and China means maintaining multiple compliance playbooks, which adds cost and complexity regardless of which jurisdiction's standards a company uses as its baseline.

Financial Services: Where AI Governance Gets Specific

For NeuroNomixer's readers in finance and risk, the intersection of the AI Act with existing financial regulation is particularly consequential.

The European Banking Authority's 2025 mapping exercise concluded that no significant contradictions exist between the AI Act and current banking legislation. This is good news for compliance teams: the AI Act is complementary to, rather than in conflict with, existing prudential frameworks. The ECB's supervision newsletter confirmed that supervisory approaches will work within existing prudential frameworks, incorporating AI-specific expectations gradually.

But complementary does not mean simple. Financial institutions deploying AI in credit scoring, fraud detection, or customer assessment must comply with the AI Act's high-risk requirements while simultaneously meeting the Digital Operational Resilience Act (DORA), ECB model risk management expectations, and existing EBA guidelines on loan origination. As we detailed in our analysis of explainable AI in credit risk, banks face a layered regulatory regime where explainability is the common thread across all frameworks.

The practical challenge is dual compliance: ensuring that AI systems meet both financial regulatory standards and AI Act requirements without duplicating documentation, testing, and governance processes. The Omnibus proposal attempts to address this by aligning overlapping requirements, but until it passes, financial institutions must plan for the current framework.

What Comes Next: The 2026-2027 Roadmap

The regulatory landscape will continue evolving. Several developments in the next twelve to eighteen months will determine whether the current framework succeeds or requires further adjustment.

The Immediate Horizon

The Commission's guidelines on high-risk AI classification, originally due by February 2026, are overdue and expected imminently. The final Code of Practice on transparency for AI-generated content is scheduled for June 2026. The Digital Omnibus proposal continues through trilateral negotiations, with the outcome likely shaping whether August 2, 2026 remains the operative deadline or shifts to late 2027.

Standards Development

The first harmonised standard (prEN 18286) is now in public inquiry, with more standards for data governance, transparency, and human oversight expected in 2026 and 2027. As these standards mature, compliance becomes more repeatable and cheaper, reducing the per-unit cost burden that currently disadvantages smaller companies.

The Liability Frontier

The revised Product Liability Directive, adopted in March 2024 and awaiting Council approval, will explicitly cover AI-related harms once finalised. This adds a new dimension: not just regulatory fines for non-compliance but civil liability for AI systems that cause consumer harm. Companies will need to factor insurance costs and product design implications into their AI development processes.

Sector-Specific Guidance

Finance-specific guidelines from the Commission were due by February 2, 2026, with EBA implementation following. Other sectors, including healthcare, education, and critical infrastructure, will likely receive tailored guidance in 2026 and 2027. For companies operating across sectors, this means compliance requirements will become more specific but also more actionable as general principles translate into sector-specific standards.

Conclusion: The Question Is Not Whether to Regulate, but How

Europe's AI governance experiment is the most ambitious regulatory undertaking in technology since GDPR. The EU AI Act, combined with the GDPR, DORA, and sector-specific frameworks, creates the most comprehensive set of AI rules anywhere in the world. Whether this comprehensive approach proves to be a competitive advantage or a competitive burden will be determined by what happens after August 2, 2026.

The evidence so far is genuinely mixed. Investment is growing (75 percent year-over-year), but the gap with the US remains enormous (six-to-one). Companies are adapting rather than leaving, but talent flows are concerning. Compliance costs are real, but so is the trust that clear rules can build. The innovation debate is not a binary: regulation imposes costs and creates opportunities, and the balance varies by company size, sector, and stage.

What is clear is that AI governance is not going away, in any jurisdiction. The US may pursue deregulation at the federal level, but state laws and public pressure ensure that governance questions persist. The UK may offer a lighter touch, but sector regulators are still applying AI-relevant standards. And the EU, despite facing legitimate criticism about compliance costs and implementation speed, is the only major jurisdiction that has established a comprehensive, enforceable framework.

For companies, the strategic imperative is to treat compliance as investment, not overhead. The institutions that build governance capacity now will move faster when standards are finalised, face lower costs when enforcement intensifies, and earn the trust that consumers and enterprise customers increasingly demand. As we argued in our manifesto for what NeuroNomixer stands for, understanding the systems that shape innovation, regulation, governance, and technology together is not optional for anyone building in this space.

The next eighteen months will determine whether Europe's regulatory bet pays off. We will be tracking every development.

Continue Reading

• The EU AI Act in 2026: What It Actually Means for Business and Innovation for the detailed requirements and compliance framework

• Explainable AI in Credit Risk: Why Banks Cannot Afford Black Boxes for how financial services are navigating dual AI governance

• Industry 5.0 Explained: Why the Future Is Human-Centred, Not Just Automated for the broader context on human-centred technology governance