What You Will Learn in This Post

This post introduces Industry 5.0: the European Commission's framework for building industries that are human-centred, sustainable, and resilient. You will learn what the framework actually says, how it differs from Industry 4.0, why the financial services sector has largely ignored it, and why that is about to change. We will also examine the legitimate criticism that Industry 5.0 is just a buzzword, and explain why the underlying principles matter for anyone working in finance, governance, or risk.

The Question Manufacturing Asked First

Financial institutions are automating decisions at an extraordinary pace. Credit scoring, fraud detection, anti-money laundering, insurance underwriting: algorithms now handle tasks that once required entire departments. But a question that manufacturers started asking five years ago is only now reaching the boardrooms of banks and insurers. It is a simple question, but the answer reshapes everything.

The question is not can we automate this? The question is: should we, and if so, how do we keep humans at the centre of the process?

In 2021, the European Commission published a framework that attempts to answer that question. They called it Industry 5.0. The manufacturing world has been debating it ever since. The finance world, by and large, has not noticed. That is a problem, because Industry 5.0's three pillars, human-centricity, sustainability, and resilience, describe exactly what regulators, customers, and risk professionals are demanding from financial services in 2026.

This post explains what Industry 5.0 is, why it matters to finance, and why it deserves your attention before August 2, 2026, when the EU AI Act's core obligations for high-risk systems become enforceable.

What Is Industry 5.0?

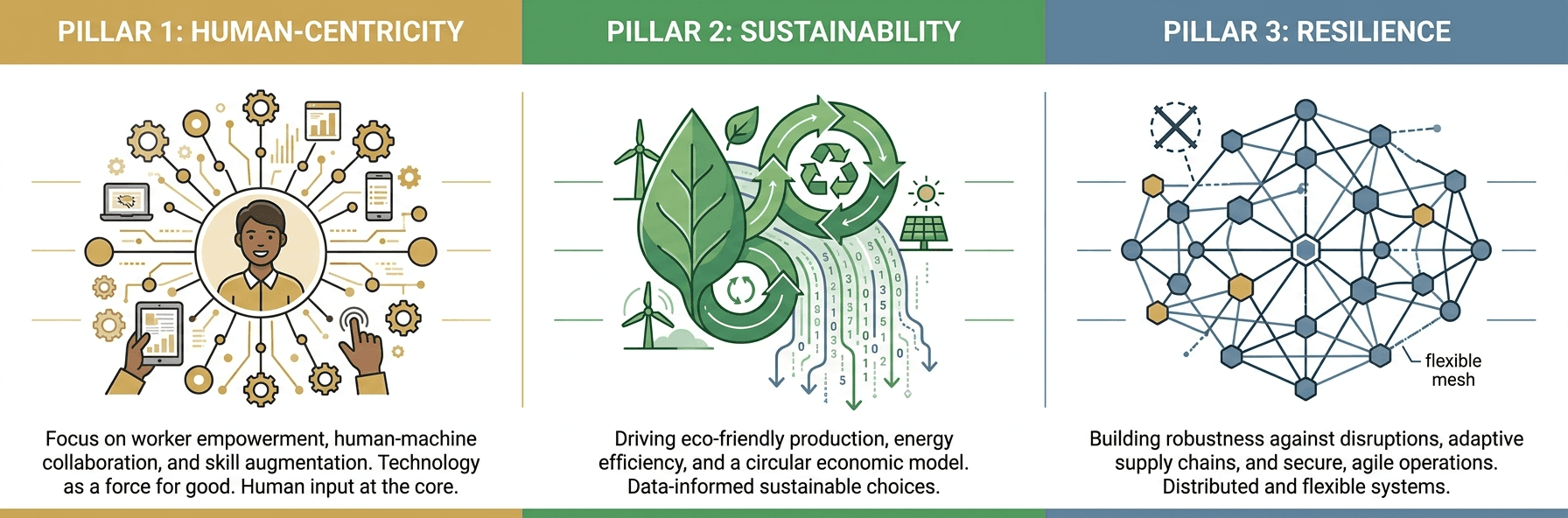

Industry 5.0 is the European Commission's 2021 framework for redefining industrial activity around three pillars: human-centricity, sustainability, and resilience. It places, in the Commission's own words, the wellbeing of the worker at the centre of the production process while using new technologies to provide prosperity beyond jobs and growth, respecting planetary boundaries.

The framework is not a replacement for Industry 4.0. It is an extension. Industry 4.0 gave us the infrastructure: the Internet of Things, cloud computing, big data analytics, and artificial intelligence. Industry 5.0 asks what we should do with that infrastructure. Where Industry 4.0 asked "What can we automate?" Industry 5.0 asks "What can technology do for humans?"

That shift in framing may sound subtle, but it changes how organisations design systems, measure success, and govern technology. It moves the conversation from pure efficiency to value, resilience, and human judgment.

The market is responding. According to Fortune Business Insights, the Industry 5.0 market reached USD 87.63 billion in 2025 and is projected to grow at a compound annual growth rate of 31.59%, reaching USD 1.04 trillion by 2034. Finland is leading the way, with approximately $3.6 billion allocated through 2027 for research, technology, climate, and workforce development. Over 100 European innovation ecosystem stakeholders participate in the EU's Community of Practice 5.0, which published its final report in October 2024.

The Three Pillars of Industry 5.0

Everything in the Industry 5.0 framework flows from three interconnected pillars. Understanding each pillar individually matters, but understanding how they reinforce each other matters more.

Human-Centricity: People as Creative Agents, Not Replaceable Resources

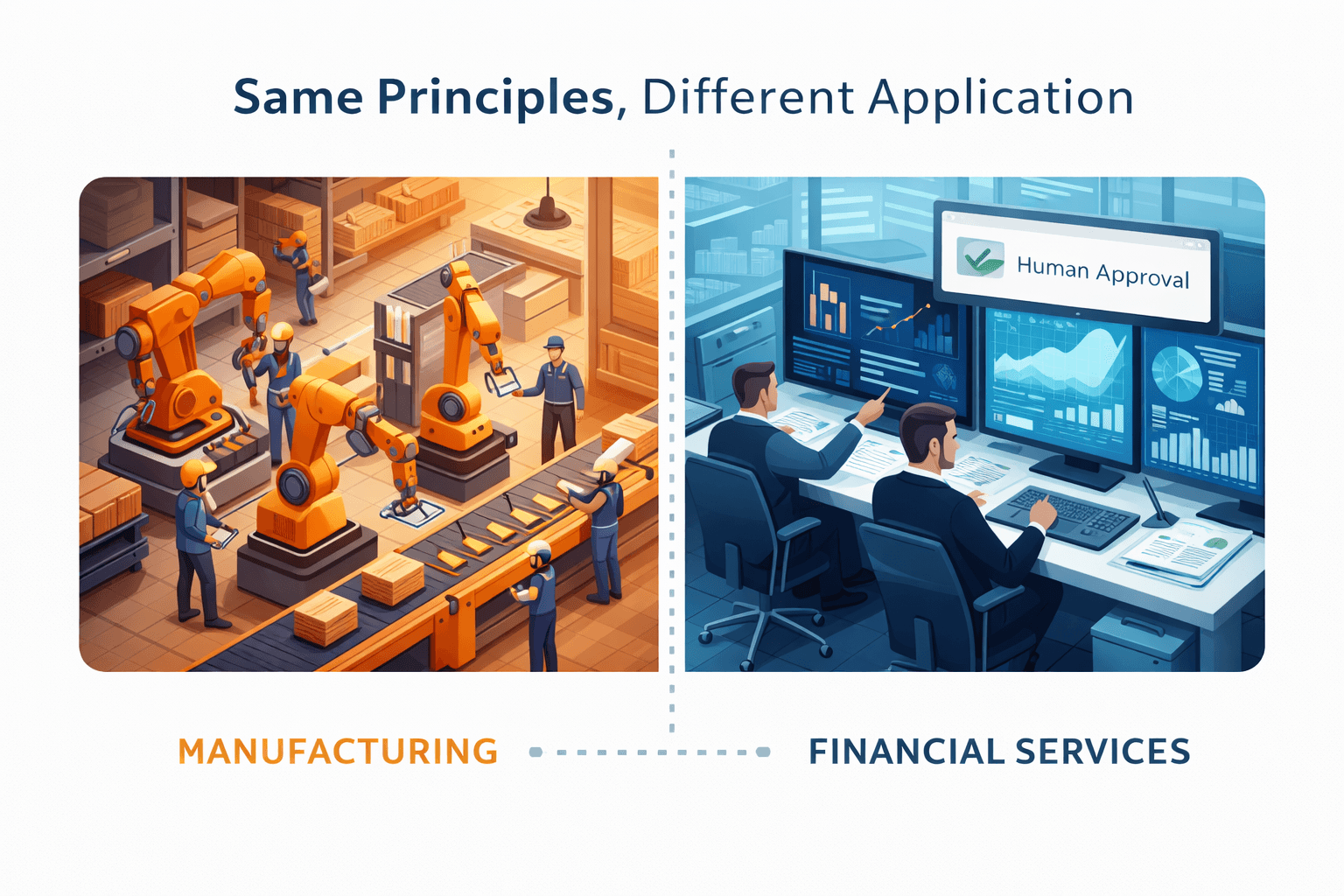

The first pillar repositions humans from passive participants in automated processes to active, creative agents who direct and oversee technology. In manufacturing, this takes the form of collaborative robots (cobots) that work alongside humans rather than replacing them. Companies like BMW and Toyota use cobots in assembly to handle ergonomically demanding tasks while human workers focus on precision, quality judgment, and problem-solving.

The principle extends beyond the factory floor. In healthcare, AI-assisted robotic surgery combines machine precision with human expertise, placing the surgeon's judgment at the centre. In every domain, the core philosophy is augmentation rather than replacement: design technology that makes human judgment better, not irrelevant.

For financial services, the implications are significant. Human-centricity means designing AI systems where algorithms suggest and humans approve, where risk models flag and experienced professionals interpret, where compliance tools monitor and analysts apply contextual judgment. It means treating "human-in-the-loop" governance not as a compliance checkbox but as a design principle.

Sustainability: Production Within Planetary Boundaries

The second pillar requires production systems built on renewable energy, circular processes, and respect for planetary limits. The European Union's carbon reduction target of 55% by 2030 is the policy backdrop, but the pillar goes deeper. It asks organisations to think beyond quarterly extraction and toward long-term alignment with the systems that sustain economic activity.

In manufacturing, sustainability means renewable energy integration, waste reduction, and recycling. In financial services, the equivalent is the integration of environmental, social, and governance (ESG) criteria into every layer of decision-making: portfolio management, lending practices, insurance underwriting, and regulatory reporting. As ESG reporting requirements tighten across the EU, the sustainability pillar provides an operational framework for what many institutions are already required to do.

Resilience: From Survival to Anti-Fragility

The third pillar is perhaps the most important for finance. Resilience, in the Industry 5.0 framework, goes beyond surviving disruption. It describes anti-fragility: the capacity to grow stronger through adversity, not merely endure it. This means supply chains, workforces, and organisations that adapt, learn, and improve when stressed.

For financial institutions, this is not abstract. Systemic resilience, the ability to prevent cascading failures, is the central concern of every central bank and financial regulator. The 2008 financial crisis, the COVID-19 market shock, and the 2023 banking tremors all demonstrated what happens when systems lack distributed, human-centred resilience. Industry 5.0's resilience pillar offers a structured framework for what regulators have been demanding: systems that combine technological capability with human oversight, distributed decision-making, and the capacity to function under stress.

How the Pillars Reinforce Each Other

The three pillars are not independent objectives; they are mutually reinforcing. Human-centricity enables resilience because diverse human judgment improves adaptability. Sustainability requires human ingenuity because automation alone cannot navigate the trade-offs of long-term thinking. Resilience depends on both human oversight and sustainable practices because brittle, short-term systems cannot withstand the disruptions that define modern markets.

When a bank designs an AI credit-scoring system with human oversight, uses it to assess climate risk in its lending portfolio, and builds fallback processes that function when the model fails, it is practising all three pillars simultaneously, whether or not it uses the Industry 5.0 label.

How Industry 5.0 Differs from Industry 4.0

| Dimension | Industry 4.0 | Industry 5.0 |

| Core Question | What can we automate? | What can technology do for humans? |

| Worker Role | Subject to automation | Central creative agent, augmented by technology |

| Value Measure | Efficiency and profitability | Profitability, societal impact, and sustainability |

| Sustainability | Secondary consideration | Core pillar |

| Manufacturing | Standardisation and mass production | Personalisation and mass customisation |

| Relationship | Foundation layer | Extends and complements 4.0; does not replace it |

The key distinction is philosophical, not technological. Industry 5.0 does not introduce new technologies so much as it asks different questions about the technologies Industry 4.0 already deployed. A comprehensive comparison by Rutgers Engineering frames it clearly: Industry 4.0 standardises; Industry 5.0 personalises. Industry 4.0 optimises processes; Industry 5.0 optimises outcomes for people.

This distinction matters enormously in finance, where the question is not whether to deploy AI, but how to deploy it in ways that maintain trust, ensure human oversight, and produce outcomes that serve customers and society rather than just shareholders.

Why Financial Services Has Not Noticed

Search for "Industry 5.0" and the results are overwhelmingly about manufacturing. Cobots on assembly lines. Digital twins in warehouses. Renewable energy in factories. More than 90% of existing content focuses on manufacturing and logistics, which makes sense: Industry 5.0 was born from the European Commission's industrial research and innovation programme, and manufacturing is where the EU's economic strategy lives.

But the absence of financial services from the Industry 5.0 conversation is a blind spot, not a design choice. Financial services is arguably the sector where Industry 5.0's pillars matter most:

• Systemic risk: Financial failures cascade. When a bank fails, it does not just affect shareholders; it threatens the entire system. Resilience in finance is existential, not operational.

• Human judgment in high-stakes decisions: Credit approvals, fraud investigations, and compliance determinations all involve nuance that algorithms handle poorly. Human-centricity is not a luxury; it is a regulatory and ethical requirement.

• Regulatory pressure: The EU AI Act, ESG reporting mandates, GDPR, and DORA (Digital Operational Resilience Act) collectively create exactly the governance framework that Industry 5.0 describes. Financial institutions are already required to be human-centred, sustainable, and resilient. They just do not call it Industry 5.0.

• Trust: Banking depends on trust between institutions and customers, between algorithms and the humans who oversee them, between regulators and the organisations they supervise. Industry 5.0's emphasis on transparency and human oversight directly addresses this.

The gap is not that finance is exempt from Industry 5.0's principles. The gap is that nobody has connected the framework to the sector that needs it most.

The Three Pillars Applied to Financial Services

If Industry 5.0's pillars were designed for manufacturing, what do they look like when applied to banking, insurance, and financial governance? The translation is more natural than you might expect.

| Pillar | Manufacturing Application | Financial Services Application |

| Human-Centricity | Cobots augment workers; ergonomic design; worker well-being | Human oversight of AI decisions; trust-building with algorithms; staff expertise valued over automation |

| Sustainability | Renewable energy; circular economy; waste reduction | Green finance; ESG integration; carbon accounting in portfolios; long-term thinking over quarterly extraction |

| Resilience | Supply chain adaptation; organisational survival | Systemic resilience; distributed decision-making; crisis preparedness; anti-fragility under stress |

Human-Centricity in Banking

In a human-centred bank, AI handles execution and humans retain authority over judgment. Credit-scoring algorithms provide recommendations; experienced analysts approve or override them with documented reasoning. Fraud detection systems flag anomalies; investigators determine context. Compliance tools monitor transactions; specialists interpret the grey areas where regulation meets commercial reality. This is "human-in-the-loop" governance, and it is both an Industry 5.0 principle and a regulatory expectation.

Human-centricity also means designing automation that enriches work rather than hollowing it out. When AI handles the routine, human professionals can focus on the complex, the ambiguous, and the empathetic: the tasks that build trust and generate the most value.

Sustainability in Finance

For financial institutions, sustainability is not optional. ESG assessment is becoming a regulatory requirement across the European Union. Carbon accounting in portfolio management, climate risk modelling in lending, and sustainable fintech innovation are moving from differentiators to table stakes. Industry 5.0's sustainability pillar provides an operational framework for these obligations, connecting environmental responsibility to the broader goal of prosperity within planetary boundaries.

Resilience in Finance

This is where Industry 5.0's framework is most powerful for finance. Financial resilience means avoiding cascading failures, maintaining distributed decision-making so that no single algorithmic failure brings down the system, and building crisis preparedness that relies on human judgment in unprecedented situations. It means designing systems that learn from stress rather than simply surviving it.

The OECD's 2020 outlook on sustainable finance highlighted that COVID-19 exposed the fragility of financial systems optimised for efficiency over resilience. Industry 5.0's resilience pillar offers a structured response: build systems that combine technological capability with human oversight, distributed architecture, and the capacity to function under conditions the models did not predict.

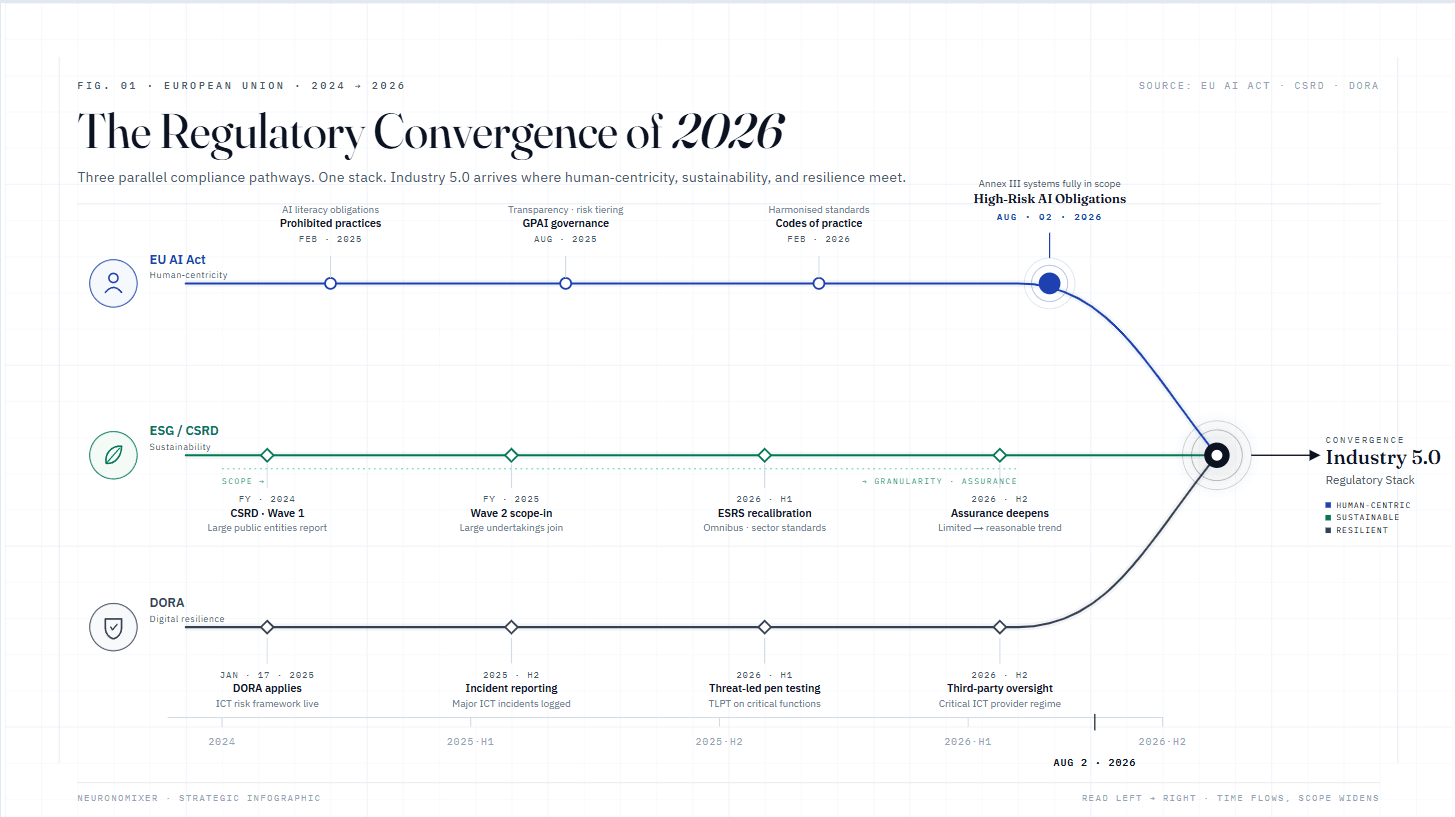

The Regulatory Alignment: Why Industry 5.0 Matters Now

The timing is not coincidental. The regulatory environment in 2026 is converging on exactly the principles Industry 5.0 describes.

The EU AI Act becomes enforceable for high-risk AI systems on August 2, 2026. Financial services AI, including credit scoring, fraud detection, and insurance underwriting, falls squarely in the high-risk category. The Act requires transparency, explainability, human oversight, and accountability at senior management level. These are Industry 5.0's human-centricity pillar expressed as law.

ESG reporting mandates are tightening across the EU, requiring financial institutions to integrate sustainability into governance, risk, and disclosure. This is Industry 5.0's sustainability pillar expressed as regulation.

DORA (Digital Operational Resilience Act) requires financial entities to build operational resilience in their digital infrastructure. This is Industry 5.0's resilience pillar expressed as a financial services directive.

Taken together, the EU AI Act, ESG requirements, and DORA create what we have previously called the "regulatory stack": overlapping mandates that collectively demand exactly what Industry 5.0 prescribes. Financial institutions preparing for compliance should recognise that they are, in effect, preparing for Industry 5.0, whether or not they use the term.

The Honest Assessment: Is Industry 5.0 Real or Just a Buzzword?

Any serious discussion of Industry 5.0 must address the criticism. And the criticism is legitimate.

Prominent voices in the Industry 4.0 community, including Germany's government-backed Plattform Industrie 4.0, argue that Industry 5.0 is rebranding, not revolution. Their position is straightforward: human-centricity, sustainability, and resilience were always part of Industry 4.0's broader vision. Calling them "5.0" is a marketing exercise, not a paradigm shift.

They have a point. A systematic review of 98 academic papers on Industry 5.0 found a lack of unified definition, poorly integrated core themes, and a shortage of rigorous quantitative research. The acceleration of "industrial revolutions", from 90 years for the first to roughly 5 years for the latest, does look more like a marketing cycle than genuine paradigm shifts.

And the implementation reality is sobering. According to Fortune Business Insights, only one-third of organisations report mature digital twin implementations, cobot adoption sits at approximately 50%, and 46% of organisations lack specific training programmes for their workforce. Implementation costs are high, ROI metrics are weak (productivity gains of 20 to 25%), and adoption barriers are real.

What is real: The EU government investment ($3.6 billion from Finland alone), the market growth (31.59% CAGR), the active pilot programmes across Europe (100+ stakeholders in CoP 5.0), and the company implementations (BMW, Toyota, ABB) are not hype. The underlying drivers, automation costs dropping, AI capability rising, sustainability pressures increasing, are structural, not cyclical.

What is uncertain: Whether "Industry 5.0" as a label will persist, whether the definitional gaps will be resolved, and whether the framework will achieve the consensus that Industry 4.0 built over a decade.

For manufacturing, the debate is about terminology. For financial services, it is about substance. The principles Industry 5.0 describes, human oversight, sustainability, systemic resilience, are not optional for regulated institutions. They are legal obligations. Whether you call it Industry 5.0 or simply good governance, the direction is the same.

Where to Go from Here

Industry 5.0 is not a technology to deploy. It is a framework for thinking about what technology should do for people, institutions, and systems. For financial services, it provides a structured way to approach the governance, sustainability, and resilience challenges that regulators, customers, and markets are demanding.

This post has established the foundation. In future posts, we will explore how the three pillars apply in practice to banking, insurance, and financial governance. We will examine how the EU AI Act's transparency requirements align with human-centred design. We will look at what systemic resilience means for financial institutions navigating an era of agentic AI, and how sustainable finance connects to Industry 5.0's vision of prosperity within planetary boundaries.

The financial services sector has been building Industry 5.0 principles into its operations for years without using the label. The question now is whether the label, and the framework behind it, can help institutions do it more deliberately, more coherently, and more effectively.

If you work in finance, governance, or risk, Industry 5.0 is not a manufacturing trend to watch from the sidelines. It is the framework for the decisions you are already making.

Explore More on NeuroNomixer

• For a deeper look at explainability requirements: Why Explainable AI Matters More Than You Think

• For the EU AI Act's full regulatory breakdown: The EU AI Act in 2026: What It Actually Means for Business and Innovation

• For how ML and analytics shape finance: Exploring How Machine Learning and Analytics Shape the Future